The Token Dollar

Oil is scarce because of war. Tokens are scarce because of physics.

Good morning. It’s the weekend. Pour yourself a cup of coffee and settle in.

Here’s the argument: AI compute may be becoming to the dollar what oil was for the last fifty years.

Oil scarcity is geopolitical. Compute scarcity is industrial. One can ease with diplomacy. The other runs into fabrication limits, memory bottlenecks, packaging constraints, power shortages, and software lock-in.

That distinction matters more than most macro investors realize — especially this week.

The world has more oil than it knows what to do with. It does not have enough tokens.

Brent crude has surged above $100. The Strait of Hormuz is effectively closed. The IEA has described the disruption as the largest in the history of the global oil market, with crude and product export flows from the Gulf reduced by millions of barrels per day. This is what vulnerability looks like when your economic leverage depends on a physical chokepoint that someone else can close. The petrodollar system — the foundation of American financial power for fifty years — is being stress-tested in real time.

Jonathan Ross posted a thread this week arguing that AI compute is replacing oil as the resource that forces the world to transact in dollars. Ross created the Google TPU, founded Groq, and joined NVIDIA through the approximately $20 billion Groq licensing-and-talent deal in late 2025, where he now leads inference architecture. His frame is directionally right but incomplete. He names the destination without mapping the mechanism.

The mechanism is what matters. The Token Dollar thesis is simple: if the world’s most important new industrial input is AI compute, and the chokepoints that produce it are priced in dollars, then rising global demand for compute reinforces dollar demand the way oil once did. The difference is that the compute chokepoint stack is more concentrated than oil ever was, the demand curve is self-reinforcing through Jevons paradox dynamics, and there is no strait that anyone can close.

Oil scarcity is often geopolitical and reversible. Compute scarcity is industrial and slower to relieve. That distinction is about to matter a great deal.

Three things converged this week that pushed me to write this piece. The MLPerf v6.0 results showed the same NVIDIA hardware producing 2.7x more tokens through software alone — confirming that the token cost curve is deflating even faster than the hardware cycle implies. Ross’s thread named the geopolitical implication nobody in macro is framing. And some proprietary data work I’ve been doing on token unit economics keeps pointing to the same conclusion: the dollar-denominated compute supply chain is creating structural demand at a scale that rivals oil.

What the Petrodollar Actually Was

Most people get the petrodollar wrong. It wasn’t a single deal. It was a system.

After Nixon ended dollar-gold convertibility in August 1971, the dollar needed a new anchor. Henry Kissinger and Treasury Secretary William Simon brokered the framework with Saudi Arabia in 1974: the Saudis would price oil in dollars and invest their proceeds in US Treasuries. In exchange, they got military protection and economic partnership. By 1975, all OPEC nations priced oil in dollars.

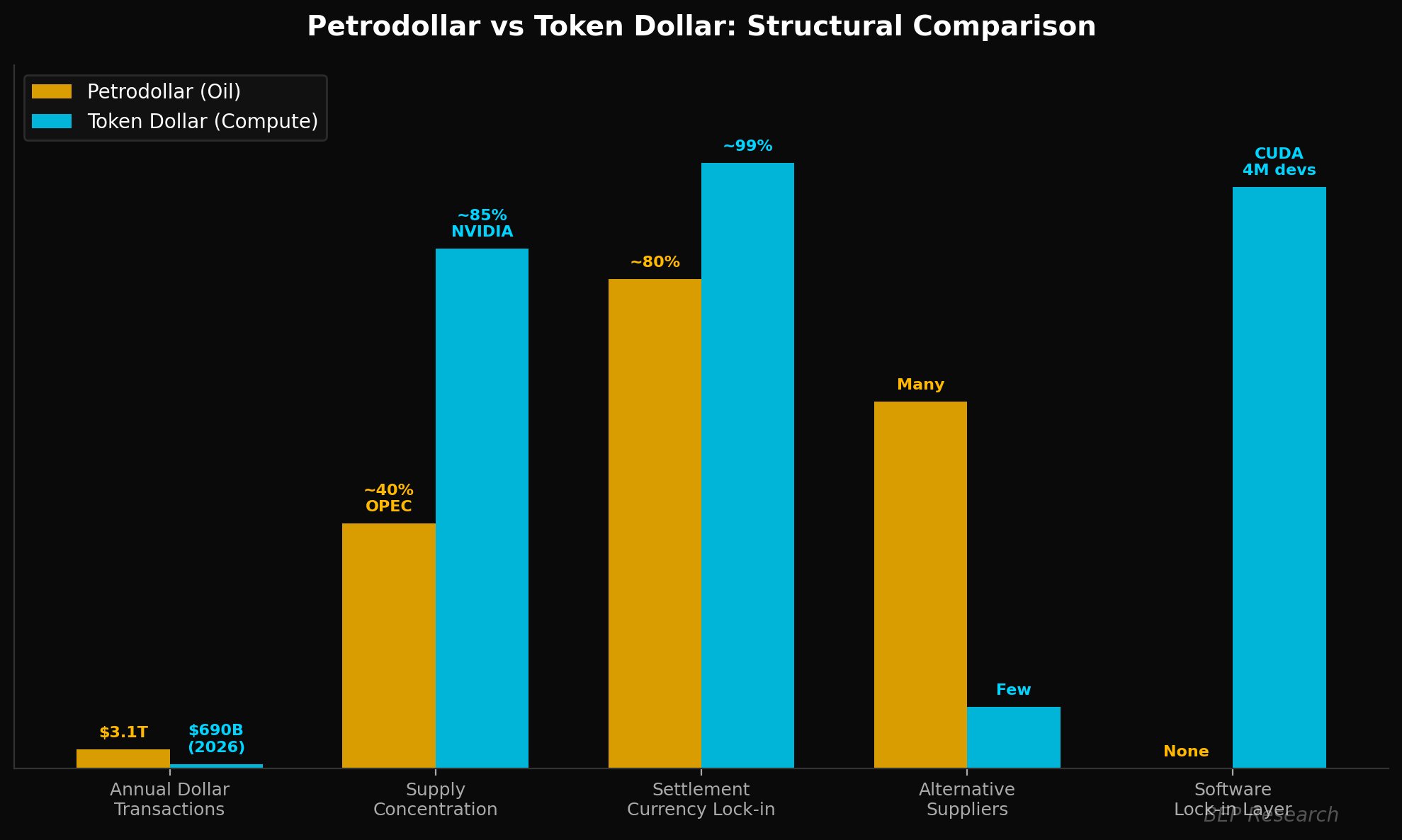

The result was elegant and self-reinforcing. Because oil traded in dollars, every country on earth needed dollars to fuel its economy. That structural demand allowed the US to run persistent deficits at artificially low borrowing costs — what Valéry Giscard d’Estaing called the “exorbitant privilege,” estimated at $50–100 billion annually in reduced financing costs. Roughly 80% of global oil trade — approximately $3.1 trillion per year — generated continuous dollar demand.

That system is now fraying. The dollar’s share of global foreign exchange reserves has declined from a peak of 72% in 2001 to approximately 57% in Q3 2025. Saudi Treasury holdings rank only 17th globally. Gulf sovereign wealth funds have shifted from Treasuries to equities. Brad Setser, the former Treasury economist, documents that petrodollar flows have “more or less dried up” at current oil prices.

Yet dollar dominance persists through sheer institutional inertia. The BIS 2025 Triennial Survey shows the dollar involved in 89% of all forex transactions. The network effects — deep capital markets, rule of law, unmatched liquidity — remain formidable even as the commodity that once underpinned them weakens.

The question is whether a new commodity is emerging to fill that role.

The Compute Chokepoint Stack

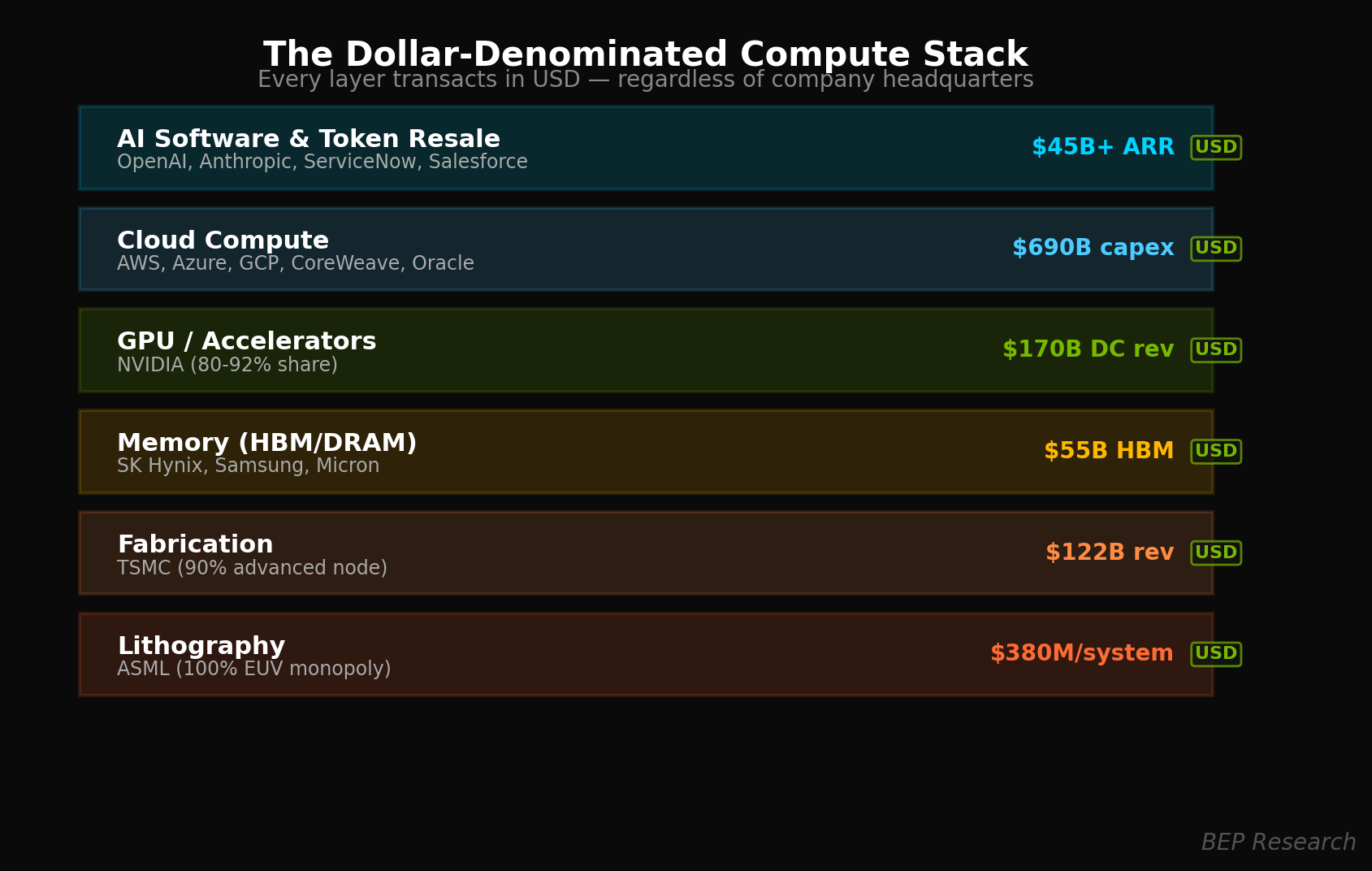

Here’s why the Token Dollar thesis is more than an analogy. The entire AI compute supply chain is denominated in dollars and controlled by American or American-aligned entities. And the concentration is more extreme than oil ever was.

I want to be precise about what “American-controlled” means here — because the obvious objection is that TSMC is Taiwanese and SK Hynix is Korean. That’s true. But the Token Dollar thesis doesn’t require every company to be headquartered in America. It requires every transaction to settle in dollars. And they do. TSMC prices exclusively in USD. SK Hynix sells HBM in dollars. ASML sells EUV systems in dollars. The entire supply chain, regardless of where a company’s headquarters sits, transacts in American currency.

Oil could be drilled in Nigeria, Venezuela, Russia, Saudi Arabia. The production base was geographically distributed even if pricing was dollar-denominated. AI compute has no equivalent distribution. The chokepoint architecture runs through a handful of companies:

NVIDIA holds an estimated 80–92% of the AI accelerator market by revenue. Broadcom controls approximately 60% of the custom ASIC co-design market. TSMC manufactures roughly 90% of the world’s most advanced AI chips. ASML holds a 100% monopoly on EUV lithography — without which advanced fabrication is impossible. SK Hynix and Micron dominate High Bandwidth Memory, with the HBM market projected to reach approximately $55 billion in 2026.

And then there’s the software layer — which has no oil-world equivalent at all.

As I wrote in The Memory Wall: “You can’t separate the silicon from the software from the model architecture.” NVIDIA’s CUDA ecosystem encompasses 4 million developers and 40,000 organizations built over nearly two decades. The integrated stack — CUDA, TensorRT-LLM, Dynamo, the proprietary NVFP4 format — creates switching costs measured in months of engineering time. This is the co-design moat I’ve been documenting across the entire series. Hardware-software co-design doesn’t just make the product better. It makes the dollar dependency structural.

Every GPU sold, every cloud instance rented, every API call made — from Mumbai to Munich to Riyadh — settles in dollars. Not because of a political arrangement like the petrodollar. Because the physics of the supply chain requires it.

CSIS published a paper in December 2025 that named this directly: the compute-dollar system offers comparable strategic advantage to the petrodollar — if the US architects it deliberately.

The World Is Short Tokens

This is where it stops being theory and starts being a market you can trade.

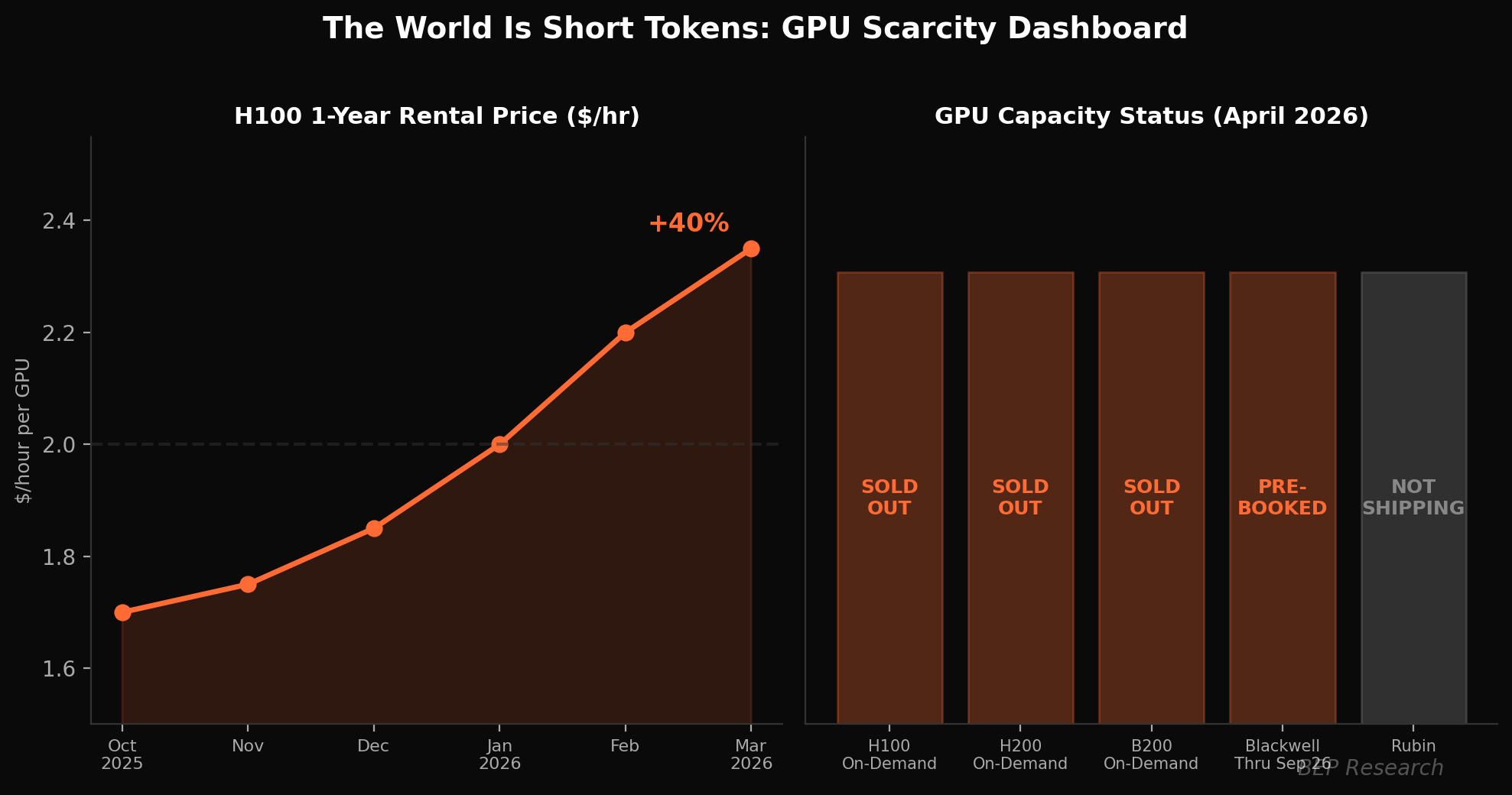

SemiAnalysis published “The Great GPU Shortage” this week documenting a market in acute distress. H100 one-year rental contract prices rose approximately 40% from $1.70/hour in October 2025 to $2.35/hour by March 2026. On-demand GPU capacity across all architectures — H100, H200, B200 — is completely sold out. Half the providers contacted for even small 64-GPU clusters had zero inventory. Some renters are subletting compute the way you’d sublet an apartment during the Monaco Grand Prix.

All Blackwell capacity coming online through August–September 2026 has been pre-booked. A reported 3.6 million Blackwell units are in the backlog. Rubin won’t ship until 2027. The supply response is measured in years, not quarters — exactly as I documented in the Micron piece when that sales leader on the LAX flight told me a decade of memory underinvestment created the imbalance.

I’ve lived this scarcity firsthand. One of my portfolio companies spent months trying to secure H100s for a training run. Not thousands of them — a modest cluster. There was simply no capacity. The waitlists were real. The broker premiums were real. And this was a company with capital ready to deploy. Multiply that experience by every AI startup, every enterprise team, every sovereign program trying to build capability, and you start to understand the structural depth of the shortage.

The existing GPU fleet is also getting more productive. As I wrote in 2.7x on the Same Iron, MLPerf v6.0 showed GB300 NVL72 delivering 2.7x higher token throughput versus its initial submissions six months earlier — same hardware, over 60% cost reduction per token, purely through software. Older Ampere-generation GPUs still see rising cloud rental prices because TensorRT-LLM and Dynamo updates keep extracting more performance. Every GPU ever deployed becomes a more productive token factory over time. And yet total demand grows faster than software can free up supply — the co-design flywheel feeding directly into Jevons.

The demand drivers are structural, not speculative. In The Token Explosion, I mapped three converging forces: reasoning models consuming 10–100x more tokens per query, agentic systems running continuously rather than in bursts, and multi-agent architectures where every sub-agent generates its own token stream. As NVIDIA VP Adel El Hallak told me at GTC: “Agents talking to agents is a lot more compute. But compute translates to tokens. Tokens translate to value. That’s why they’re calling them AI factories.”

Memory is a binding constraint. Data centers are projected to consume 70% of global memory supply in 2026. Micron discontinued its entire consumer Crucial memory lineup to prioritize AI. NVIDIA reportedly cut GeForce RTX 50 series production by 30–40% due to GDDR7 shortages. Chips, memory, packaging capacity, and power are all simultaneously constrained.

Why Falling Token Costs Strengthen the System

The obvious objection: “You can’t invoke scarcity and collapsing costs at the same time. Pick one.” That gets the causality backwards.

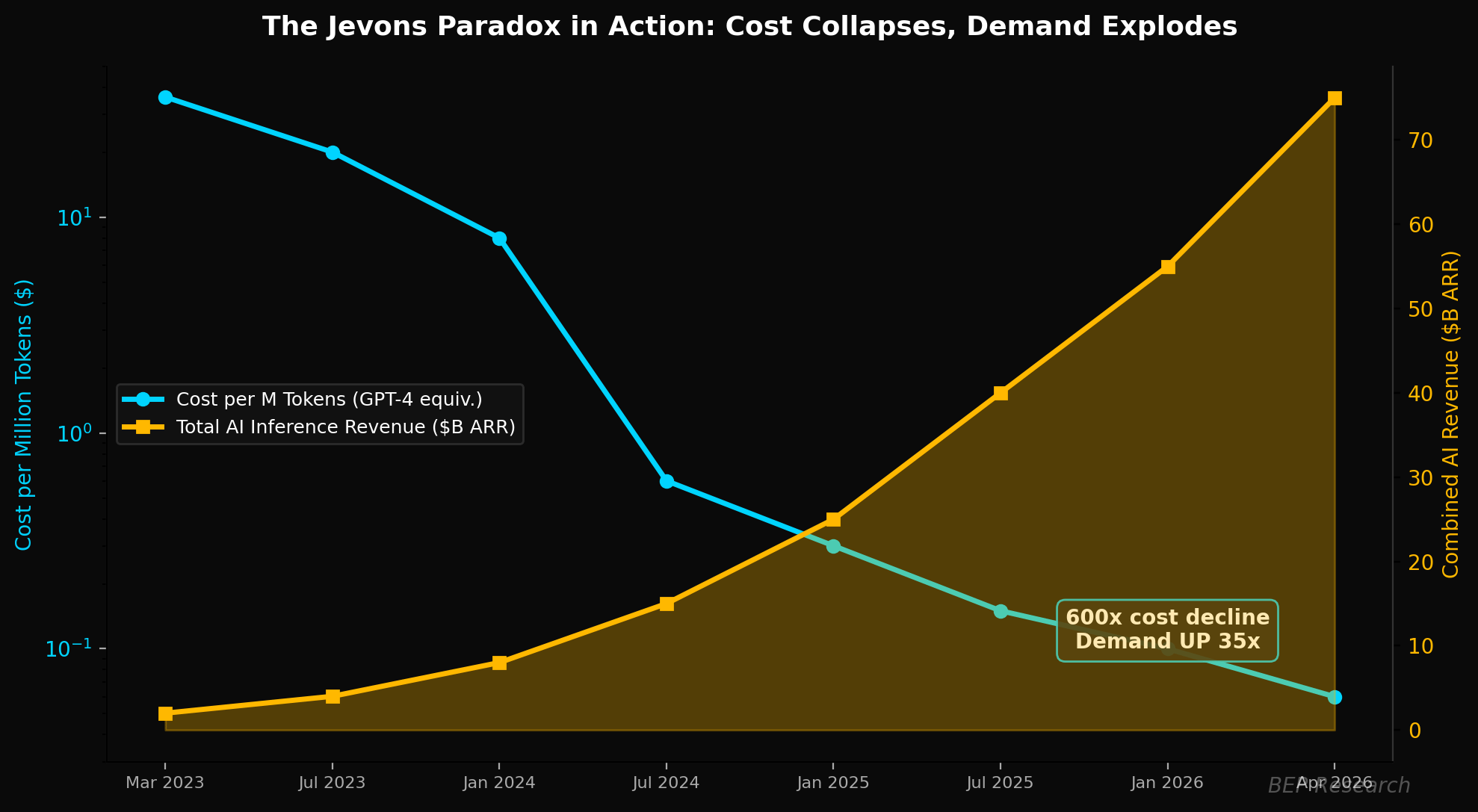

Oil’s scarcity is geological — fixed reserves, extraction bottlenecks, OPEC discipline. Compute’s scarcity is industrial — and it’s caused by the cost collapse, not contradicted by it. The 100–300x cost decline (600x if you include open-source models at the frontier) didn’t reduce GPU demand. It made demand insatiable. Cheaper tokens unlocked workloads that didn’t exist at higher prices, and those workloads consumed more total compute than the efficiency gains freed up. Different physics, same monetary result: structural dollar demand that self-reinforces.

The cost per AI token has collapsed at extraordinary rates. GPT-4 level capability that cost $36 per million tokens at launch in March 2023 dropped to $0.60 with GPT-4o mini by July 2024 — a 60x decline in 16 months. The composite decline for equivalent capability over roughly two years spans 100–300x. In any normal commodity market, this would destroy demand for the underlying infrastructure. Instead, every 10x cost reduction unlocks new workloads — agentic AI, real-time voice, media generation, autonomous coding — that consume orders of magnitude more total compute.

Anthropic’s trajectory is the clearest illustration. ARR grew from approximately $1 billion in December 2024 to an estimated $14 billion by early 2026, according to reporting from The Information — a roughly 14x increase in 14 months. SemiAnalysis reported Anthropic added roughly $6 billion of ARR in the single month of February 2026, noting that “if Anthropic had more compute they would have added more.” OpenAI reached approximately $25 billion ARR. The combined spend keeps accelerating even as per-token costs plummet.

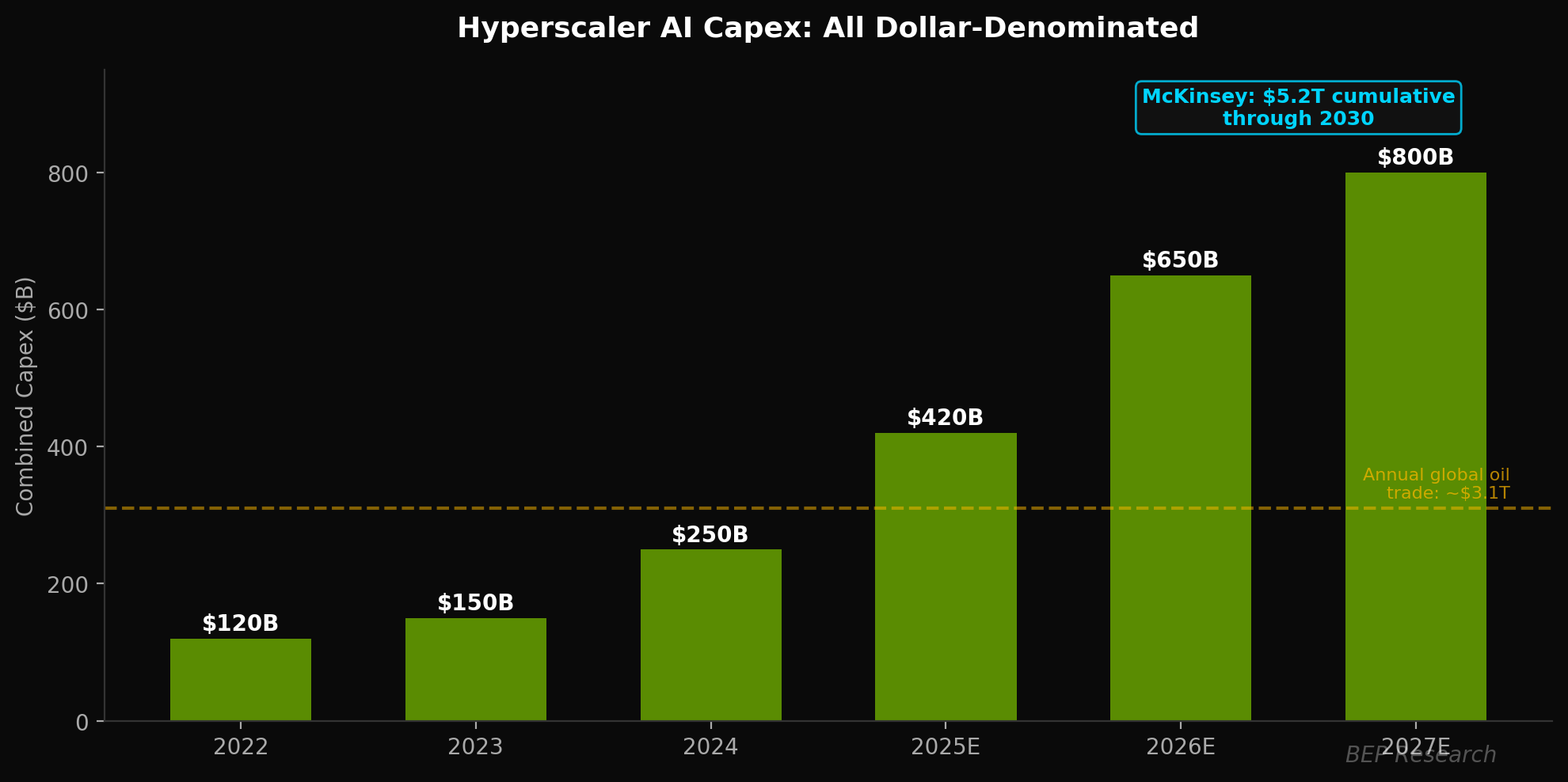

The hyperscaler capital response makes the dollar demand explicit. Combined 2026 capex for the largest cloud providers is projected at $600–690 billion — roughly 2.5x 2024 levels. Amazon guides $200 billion. Google approaches $175–185 billion. Microsoft tracks above $120 billion. Goldman Sachs projects cumulative 2025–2027 hyperscaler capex of $1.15 trillion. McKinsey’s base case calls for $5.2 trillion in AI data center investment between 2025 and 2030.

Every dollar of that capex flows through the dollar-denominated compute stack.

The Energy Wall: You Can’t Print Tokens Without Power

There’s a physical constraint underneath all of this that most macro analysts ignore: you can’t produce tokens without electricity, and electricity for AI data centers is finite.

I mapped this in detail in The Token Explosion. NVIDIA’s rack power density trajectory is relentless: 35 kW per rack with Hopper, 120 kW with Blackwell, 300 kW with Rubin, 600 kW+ with Kyber. A 17x increase in five years. The Feynman generation pushes toward 1 megawatt per rack — one rack consuming the same power as 300 American homes.

Grid interconnection queues run 5–7 years. Total US data center power consumption is estimated at 30–40 GW today and climbing fast. $64 billion in data center projects have been blocked or delayed by local opposition to power infrastructure. The token factory can’t grow faster than the power grid allows — unless you change how the factory interacts with the grid.

This is why NVIDIA’s DSX platform matters for the Token Dollar thesis. DSX Max-Q deploys 30% more AI infrastructure within a fixed-power data center through dynamic power provisioning — essentially making the AI factory smart about when and how it uses electricity. DSX Flex targets 100 GW of stranded grid power by making AI factories grid-flexible assets that can shift loads during demand response events, absorb off-peak power, and participate in grid services. For context, if DSX Flex captures even a fraction of that stranded capacity, it fundamentally changes the power constraint narrative. At GTC, NVIDIA’s Dion Harris framed this as extreme co-design extended to the building itself: “That extreme co-design is taken even a step further — not just at the chip networking computing level, but at the physical infrastructure level as well. That’s why when Jensen describes that five-layer cake, he always starts with energy.”

And as I wrote in the Bloom Energy deep dive, behind-the-meter generation solves the speed problem. Bloom’s fuel cells output 800V DC natively — no conversion required. Oracle deployed a Bloom-powered AI factory in 55 days. Traditional grid AC loses 10–12% of electricity to conversion stages before it reaches the rack. Bloom’s native DC architecture drops that to roughly 3%. At 1 megawatt per rack, that efficiency delta isn’t incremental. It’s strategic.

The energy constraint is another layer of the Token Dollar argument. The world can’t just build more token factories without solving power — and the power solutions (DSX, 800V DC, behind-the-meter generation) are themselves American technologies, priced in dollars, sold by American companies. Energy scarcity doesn’t weaken the Token Dollar. It concentrates it further.

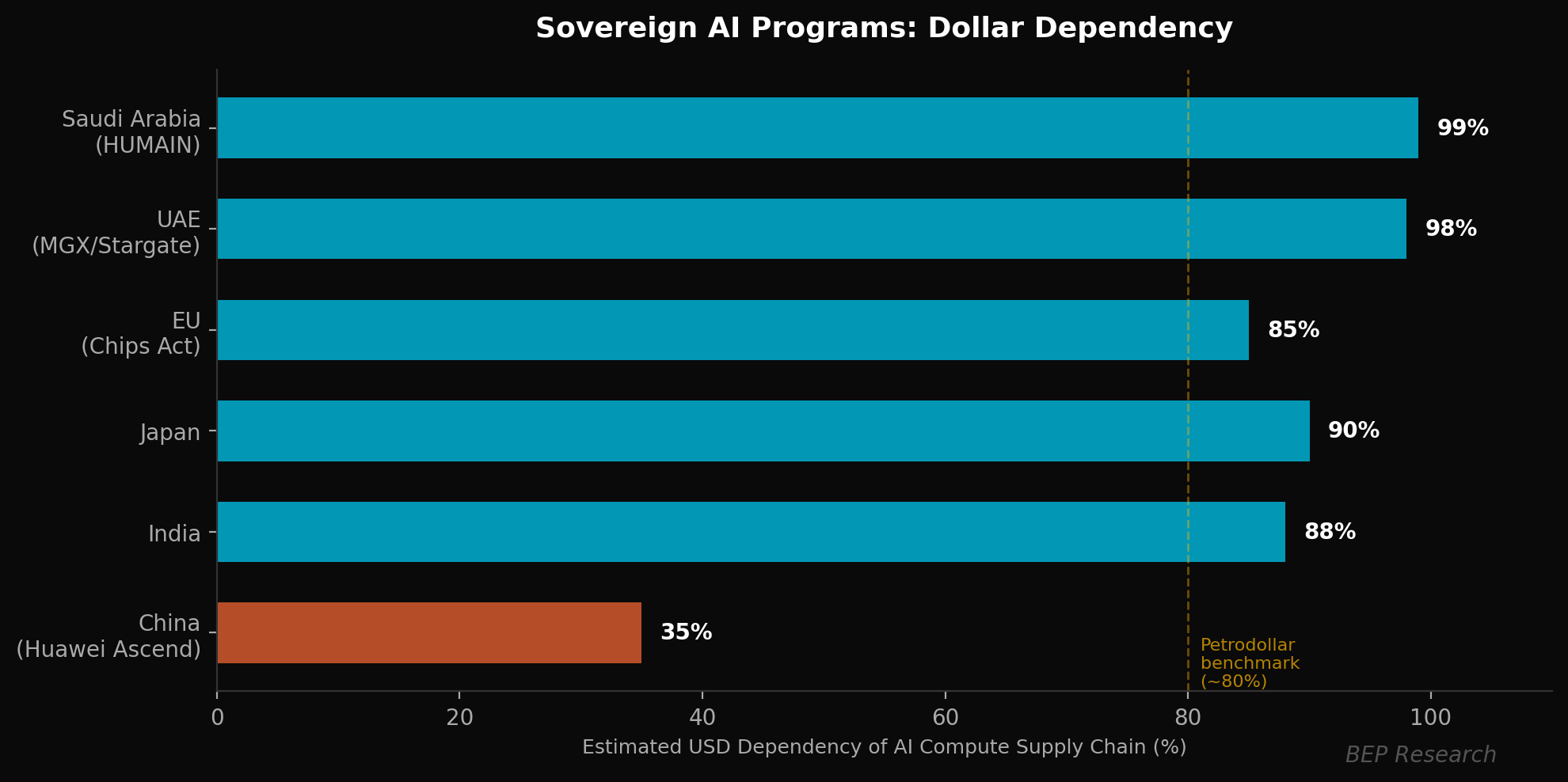

Sovereign Compute Confirms the Dependency

Sovereign AI programs universally transact in dollars despite being designed to reduce American technological dependency. Countries explicitly trying to build compute independence are deepening their dollar dependency in the process.

Saudi Arabia’s HUMAIN initiative targets 1.9 GW of compute capacity through a reported $77 billion strategy, deploying up to 600,000 NVIDIA GB300 GPUs. Aramco Digital signed a $1.5 billion partnership with Groq for what’s described as the world’s largest inference data center. Every deal — with NVIDIA, Google Cloud ($10 billion), Microsoft ($2.2 billion), AWS — is denominated in USD. The Saudi riyal’s fixed peg at 3.75 SAR/USD makes this functionally indistinguishable from direct dollar transactions.

The UAE’s MGX investment vehicle targets $100 billion in assets and anchors the $500 billion Stargate Project alongside OpenAI, Oracle, and SoftBank. G42 divested from Chinese companies specifically to maintain access to American chips. The dirham is pegged to the dollar.

Notice the pattern. The petrodollar nations — the same Gulf states that built their wealth on dollar-denominated oil — are now recycling that wealth into dollar-denominated compute. The commodity changed. The currency didn’t. One analysis captures the dynamic precisely: for every dollar the UAE invests in a Middle East data center, it must invest another dollar into US-based AI infrastructure — essentially mirroring the 1970s petrodollar recycling strategy for the AI era.

This connects directly to The NeoCloud Hypothesis, where I argued that CoreWeave and Oracle function as NVIDIA’s distribution layer. If US export policy channels foreign AI infrastructure investment through domestic NeoClouds — and the regulatory momentum suggests it will — the demand tailwind becomes structural. Oracle’s 147 sovereign cloud regions make it the natural landing pad for sovereign compute commitments that must route through the American stack.

The European Union faces the sharpest sovereignty paradox. The European Chips Act aimed to reach 20% of global semiconductor production by 2030; projections suggest approximately 12% at best, concentrated in automotive chips, not AI accelerators. Every “sovereign” European AI deployment runs on NVIDIA GPUs fabricated by TSMC. US hyperscalers control roughly 65% of the EU cloud services market. The hardware must still be purchased at USD-referenced prices regardless of what Brussels legislates.

US export controls add a political dimension absent from the petrodollar system entirely. The three-tier framework conditions chip access on geopolitical alignment — creating what one analysis described as a centrally planned global computing economy. Countries must maintain close US relationships to ensure continued access, regardless of which administration holds power. This is OPEC-style supply leverage, except the cartel is a single company’s product roadmap.

GPUs Are Becoming a Financial Asset Class — and Tokens Are Becoming the Revenue Layer

This is where it gets really interesting for anyone who remembers how oil markets evolved. We’re watching compute become a tradeable commodity in real time.

But before the financial instruments, consider what’s happening at the application layer. As I argued in Is Software Dead?, the SaaS industry is transitioning from selling seats to selling tokens. ServiceNow’s “Flex Credits,” Salesforce’s per-action pricing — every AI-native software company is becoming, at its core, a token reseller. They buy compute at wholesale, add intelligence and workflow, and sell tokens at retail. Their gross margin is the spread between what they pay for inference and what they charge the customer. That means the entire software industry is now structurally exposed to dollar-denominated compute economics.

Jensen showed this at GTC with five inference pricing tiers — from free at $0 to ultra at $150 per million tokens. That’s not a GPU pricing slide. That’s a commodity market with differentiated grades. The token is being financialized.

CoreWeave’s debt trajectory tells the story. GPU-backed facilities that priced at SOFR + 1,300 basis points in 2023 have compressed to CoreWeave’s March 2026 landmark $8.5 billion facility rated A3 by Moody’s at SOFR + 225 basis points — a spread compression of over 1,000 basis points in roughly two years. The deal was led by Blackstone, MUFG, Morgan Stanley, Goldman Sachs, and JPMorgan. Meaningfully oversubscribed.

CoreWeave itself has grown from $16 million in 2022 revenue to a guided $4.9–5.1 billion in FY2025, with over $50 billion in contracted future obligations. Its $14.2 billion in total debt is backed by 250,000+ NVIDIA GPUs — physical assets functioning as collateral the way oil reserves back energy sector financing.

Nascent compute futures markets are forming. Ornn raised $5.7 million to build a compute futures exchange. Architect Financial announced exchange-traded futures on datacenter compute. The trajectory from bilateral contracts toward standardized exchange-traded instruments mirrors exactly how oil evolved from bespoke deals into the Brent/WTI benchmark system that crystallized petrodollar pricing.

JP Morgan estimates the data center buildout will require $1.5 trillion in investment-grade bonds over five years. That’s $1.5 trillion in dollar-denominated financial instruments backed by American compute infrastructure. The Token Dollar isn’t just about GPU sales. It’s about an entire financial ecosystem denominated in dollars and collateralized by American technology.

The Bear Case

I’m making a big claim. Here’s where I could be wrong — because I don’t trust analysts who can’t articulate what breaks their own thesis.

Compute is expandable. Oil is not. New fabs can be built. Algorithmic improvements substitute for hardware. DeepSeek V3 reportedly trained on 2,048 H800 GPUs in under two months for approximately $5.6 million in compute costs, versus Meta’s Llama 3 requiring 16,384 H100s. This 11x compute efficiency gap demonstrates that software innovation can partially offset hardware scarcity. Oil has no algorithmic substitute.

Jevons doesn’t guarantee value capture by producers. Coal consumption exploded in the 19th century, but individual coal mines got commoditized. The question is whether the analogy holds for a vertically integrated platform with 80–92% market share and 75% gross margins — or whether compute follows the coal mine path toward commodity competition. My answer: value accrues to the orchestration and software layers (Dynamo, TensorRT-LLM, CUDA) where switching costs are measured in months of engineering time. Commodity hardware layers are more vulnerable. Not every infrastructure supplier wins in a Jevons world. The ones with stack depth do.

No natural dollar-settlement mechanism exists yet. CSIS explicitly identified the gap: current US-Gulf AI agreements lack any guarantee that AI-enabled exports generated using American chips will be invoiced in dollars. A country might spend $10 billion on dollar-denominated infrastructure but generate $50–100 billion annually in AI services settled in local currency. The petrodollar worked because oil is a fungible commodity traded on global exchanges with standardized benchmarks. AI compute is heterogeneous — resisting the kind of commoditization that creates benchmark pricing.

Open-source models create genuine alternatives for inference. DeepSeek, Llama, Mistral, and Qwen enable sovereign deployment on local hardware. For inference workloads — which now constitute the majority of AI compute — open-source models on non-American hardware represent a credible path to reduced dollar dependency. This is the bear case for the software layer of the thesis, even though the hardware layer remains constrained.

China is building an alternative stack, albeit constrained. Huawei’s Ascend 910C achieves an estimated 60–80% of H100 inference performance. Bernstein estimates Huawei’s share of China’s AI chip market rose to approximately 40% in 2025. But the Ascend supply chain depends on a finite stockpile of TSMC-fabricated dies, SMIC’s 7nm process yields reportedly only 30–40%, and domestic HBM capacity can support only 250,000–300,000 chips per year. CFR estimates the Chinese chip performance gap at approximately 5x today, widening to 17x by 2027. China’s domestic ecosystem is real but structurally constrained.

The analogy’s time horizon may be limited. American leverage is maximal now but could narrow over 5–10 years as Chinese capabilities mature, algorithmic efficiency reduces hardware requirements, and supply expands through new fabs. The petrodollar persisted for fifty years because oil reserves are geologically fixed. Compute capacity is an engineering problem solvable with sufficient capital and time. The strongest version of the bear case holds that the window of maximum leverage is 3–7 years.

Compute may never standardize the way oil did. The cleanest objection is that oil is a globally standardized commodity traded on benchmark exchanges, and compute is not. If AI compute never standardizes into benchmarked, fungible units — if it remains heterogeneous across architectures, workload types, and performance tiers — then the analogy stops short of true petrodollar replacement. The nascent compute futures markets are directional evidence, but they are nascent.

These are real constraints. But even “limited” leverage of 3–7 years over a market approaching $1 trillion in annual capex is an extraordinary structural position. The question for investors isn’t whether the Token Dollar dynamic exists. It’s whether the window is long enough to matter for portfolio construction.

The Investment Map

The Token Dollar thesis reinforces the same infrastructure map I’ve been building across the entire body of work — but adds a geopolitical durability layer that most semiconductor analysis ignores.

The compute stack: NVIDIA remains the center of gravity. NVIDIA data center revenue is tracking toward an estimated $170 billion in FY2026. The co-design moat — silicon plus software plus compiler plus orchestration — is the reason the dollar lock-in persists. This isn’t just a GPU company. It’s the reserve currency issuer of the compute economy.

The memory layer: Every token that runs through the system hits the memory wall I’ve been documenting since the first Co-Design Series installment. SK Hynix, Micron, and the entire HBM supply chain benefit from both the volume growth and the scarcity premium. Memory is to the Token Dollar what refining capacity was to the petrodollar — the bottleneck that concentrates pricing power.

The distribution layer: CoreWeave and Oracle, as I argued in The NeoCloud Hypothesis, are NVIDIA’s GPU distribution partners. They deploy first, they deploy fastest, and they’re increasingly the landing pad for sovereign compute commitments routed through the American stack. The NeoCloud thesis is really a Token Dollar thesis in infrastructure form.

The bandwidth layer: Every rack of Vera Rubin deployed multiplies optical interconnect demand. Lumentum, Credo, Astera Labs, Tower Semiconductor — the companies I’ve been covering across the photonic divergence and OFC field notes — are the circulatory system of the token factory. Tokens don’t just need to be produced. They need to move. And they move on dollar-denominated optical infrastructure.

The power layer: Bloom Energy, as I wrote in the earnings piece, is positioned at the intersection of compute scarcity and power scarcity. Hyperscalers spending nearly $700 billion on infrastructure this year, and the binding constraint is still power. The Token Dollar only works if the token factories have electricity — and that power infrastructure is overwhelmingly American.

Where This Goes

Global oil trade generates roughly $3.1 trillion annually in dollar-denominated transactions. Hyperscaler AI capex alone will reach an estimated $600–690 billion in 2026, growing toward $1+ trillion annually by decade’s end. McKinsey’s cumulative figure is $5.2 trillion through 2030. Add enterprise AI spending, sovereign compute programs, and the GPU-backed financial asset class, and AI compute transactions could approach oil-scale dollar demand within this decade — while the petrodollar system itself faces its most severe stress test in fifty years.

In some ways, the compute-dollar system is already more concentrated than the petrodollar ever was. Oil had OPEC, but OPEC was a cartel of competitors. The compute stack has a single dominant platform vendor with 80–92% market share, a fabrication monopoly, a lithography monopoly, and a software ecosystem with two decades of lock-in. Oil could be drilled in dozens of countries. Advanced AI chips can be fabricated in two.

The system lacks the settlement architecture and pricing benchmarks that made the petrodollar self-sustaining. But the hardware dependency is deeper, the supply concentration is tighter, and the demand trajectory is steeper. The Strait of Hormuz can be reopened. The laws of physics that constrain fabrication, memory, packaging, and power cannot be negotiated with.

I’m building something on the quantitative side that will make this framework more rigorous — more on that soon. An institutional note with the full model is coming later this quarter. If you’re an institutional reader and want early access, reach out directly.

The token factory never stops growing. And it only takes dollars.

Disclosure: I hold positions in NVDA, LITE, CRDO, ALAB, LSCC, TSEM, ORCL (2027 LEAPS), and BE. I do not hold positions in META, ARM, INTC, or AMD. This is not investment advice.

Related BEP Research

The Token Explosion: Why GTC 2026 Was Really About Building the World’s Largest Token Factory

The Memory Wars: Why NVIDIA’s 2028 Architecture Ends the AI Chip Competition

The Memory Wall: Why Groq and Jamba Had to Find Each Other (Co-Design Series Part 1)

2.7x on the Same Iron: MLPerf v6.0 Just Validated the Co-Design Thesis

Resources

CSIS: Turning the AI Revolution into Dollar Dominance (December 2025)

Dylan Patel Semianalysis: The Great GPU Shortage (March 2026)

Epoch AI: LLM Inference Price Trends

McKinsey: The Cost of Compute: A $7 Trillion Race to Scale Data Centers

BIS: 2025 Triennial Survey on FX Turnover

Probably the most insightful article I've ever read on Substack. 👍

Hey, Ben. Thanks for this piece. I have recently started to follow you on X and am now a subscriber here. You are an *original* thinker. Have not read this take anywhere else and it does make a lot of sense.

You might be years ahead of everyone!

Just one clarification, if I may. Translating compute to tokens, how does this work specifically? Example, Irene rents their gpu's likely at a fix rate via contracts. Bare metal, as their CEO likes to point at their strategy, does not seem to capture the token economy in full.

So, are the companies hosting open models that can sell "by the token" the ones who will capture the largest and the longest piece of this massive, future market (all countries on earth, all industries on earth)?