Is Software Dead? Who Survives When AI Eats the Premium?

Karpathy explains the mechanism. Chamath explains the consequence. Avenir explains why context—not code—determines who wins.

By Ben Pouladian | BEP Research

It was another busy week in AI—Anthropic released Opus 4.6 and OpenAI dropped Codex 5.3 which I will write about soon and how it relates to AI infrastructure. I’ve been working on this piece for a while and wanted to get it out before the Super Bowl. Go Patriots!!!!

A note to subscribers: The paywall goes up March 9. Watch your inbox for an early subscriber discount link.

Everyone has beaten software like a dead horse. Sorry if I am late to the party. On December 26, 2025, Andrej Karpathy posted a confession that ricocheted through Silicon Valley: “I’ve never felt this much behind as a programmer.”

This wasn’t some junior developer struggling to keep up. This was the former director of AI at Tesla, a co-founder of OpenAI, a man who can derive backpropagation on a napkin. And he was admitting that the profession of software engineering is being “dramatically refactored.”

Less than a month later, on January 21, 2026, Chamath Palihapitiya declared what the market had been whispering: “The Great SaaS Meltdown has started and there’s no going back.”

These aren’t disconnected observations. They’re two views of the same seismic shift—and the market is already pricing it in. The Avenir SaaS Index is down 27% while the Nasdaq 100 is up 50% over the same period. That’s a 77 percentage point divergence. But the real story is in the dispersion: Horizontal SaaS is down 49% while Vertical SaaS and Cyber is roughly flat.

The question every investor should be asking: Is this a buying opportunity or a value trap?

The Karpathy Confession

Let me share what Karpathy actually said, because the implications extend far beyond coding.

He described a new “programmable layer of abstraction” involving “agents, subagents, their prompts, contexts, memory, modes, permissions, tools, plugins, skills, hooks, MCP, LSP, slash commands, workflows, IDE integrations.” The profession, he wrote, is being “dramatically refactored as the bits contributed by the programmer are increasingly sparse and between.”

Karpathy coined the term “vibe coding” earlier in 2025—building software by describing what you want in English while the model handles the implementation. By year’s end, he was describing AI as “like some powerful alien tool thrown into the world without an instruction manual.”

The most provocative observation: “I have a sense that I could be 10X more powerful if I just properly string together what has become available over the last year and a failure to claim the boost feels decidedly like skill issue.”

This is the key insight. AI isn’t just making existing work faster—it’s expanding what’s economically viable to build. For SaaS companies, this cuts both ways. Your engineers might be more productive. But so are your competitors. And so are your customers’ internal teams who might decide they can build what you sell.

Meta’s Q4 2025 earnings call quantified this shift. Mark Zuckerberg reported a 30% increase in output per engineer since the beginning of 2025, “with the majority of that growth coming from the adoption of agentic coding.” Power users of AI coding tools saw output increase 80% year-over-year. “We expect this growth to accelerate through the next half.”

If Meta’s engineers are 30-80% more productive, what does that mean for the SaaS companies selling tools to less sophisticated engineering organizations?

The Great SaaS Meltdown

On January 21, 2026, Chamath Palihapitiya posted a thread on X that crystallized what the market had been pricing in for months:

His diagnosis was surgical: “In short, hi growth, low/no profitability SaaS is no longer a winning strategy because the big question mark is the durability of that growth in the short term and, because of AI, the lack of profits in the long term.”

The fundamental assumption underlying SaaS valuations—grow now, harvest later—is breaking down. As Chamath put it: “Every SaaS company has sold the dream (to investors and employees) that they will growth quickly now, and harvest lots of cash later. With AI, this assumption may be completely out the window.”

His warning for startups was particularly pointed: “If you are a venture supported SaaS startup and are a legacy Heuristics+APIs+CRUD product, it is likely that a new AI oriented workflow is coming for you.”

The narrative volatility is extraordinary. Akram’s Razor—a 25+ year market veteran who has crafted some of the best activist short and long reports on names like The Trade Desk and Sprout Social—describes going “from shorting a bunch of SaaS on ClaudeCowork to giga long some software names for a couple days and effectively back to neutral” in just two weeks. Atlassian up 20% in five days. Cloudflare up 25% in two days. “These are not meme stocks. You essentially have little time to think about a thesis as emotions really have taken over a lot of things in markets.”

Microsoft’s problem, as Akram frames it: “for the past 9 months has been that it’s not Google. And now the problem is that it’s not Google or Meta.” ClaudeCowork is “making Office look stupid.” Relatives matter more than absolutes in markets—and the relative narrative for horizontal software is brutal.

Chamath has been building toward this thesis for over a year. His 8090 incubator, launched in 2024, operates on a radical premise: tell them which enterprise software you’re using, and his team will deliver an 80% feature-complete alternative at a 90% discount using AI and offshore development.

This is a fundamental repricing of terminal value assumptions. The threshold question, as Chamath frames it: “whether their growth will be overtaken by a much cheaper AI-developed solution.”

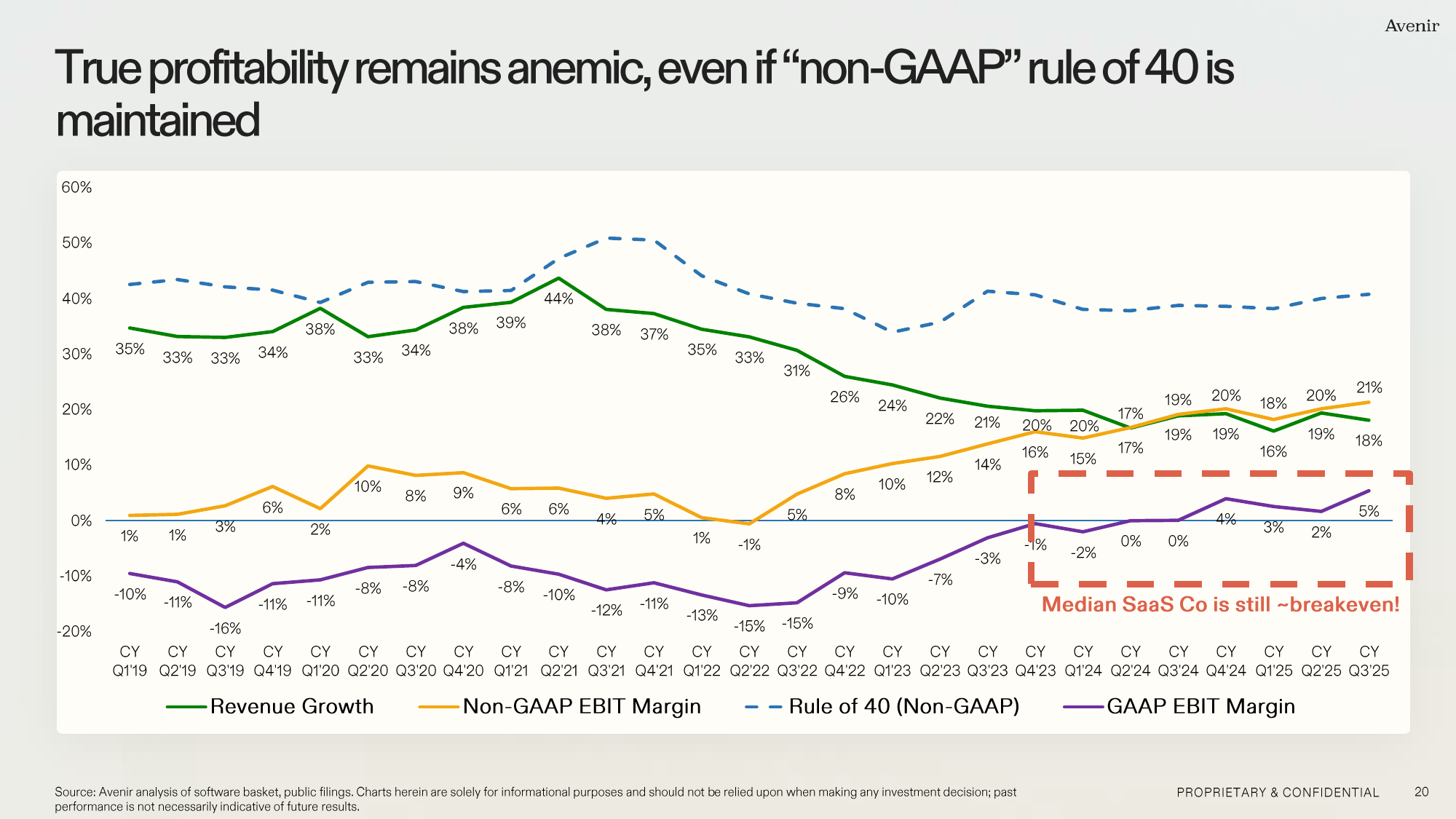

The Rule of 40 Is a Lie

Before we go further, let’s dispense with the metric that has given SaaS investors false comfort for a decade: the Rule of 40.

The Rule of 40 says a healthy SaaS company’s revenue growth rate plus profit margin should exceed 40%. It’s become the standard way to evaluate the tradeoff between growth and profitability. There’s just one problem: as implemented, it’s nearly meaningless.

The dirty secret is that most SaaS companies report Rule of 40 using non-GAAP operating margins—which conveniently exclude stock-based compensation. When you add SBC back in, the picture changes dramatically.

Source: Avenir analysis of software basket, public filings. January 2026.

The Avenir data tells the story. The median public SaaS company maintains a non-GAAP Rule of 40 score around 40%—technically healthy. But their GAAP EBIT margins hover around 5%. The median SaaS company is essentially breakeven on a real economic basis, even after a decade of supposed “scaling.”

Stock-based compensation as a percentage of revenue peaked around 20% in 2022-2023 and remains elevated at 16% today. That’s not a rounding error—it’s the entire margin profile. SaaS companies have been paying employees with shareholder dilution and calling the result “profitability.”

To their credit, some companies are getting the message. Atlassian announced this week that founders will pause their selling plans that have been in place since IPO, and the company has already repurchased more shares in January alone than all of Q2. Their shareholder letter framed it as a way “to further underscore their conviction in our massive long-term growth opportunities.” Translation: we know the SBC optics are terrible and we’re trying to offset it. But one company’s mea culpa doesn’t fix an industry-wide problem.

When Chamath says the “harvest later” assumption is breaking down, this is what he means. There was never going to be a harvest. The Rule of 40 was always an elaborate accounting fiction that let high-growth companies claim profitability they didn’t have.

AI doesn’t just threaten SaaS revenue—it exposes this fundamental weakness. If you’ve been subsidizing your workforce with equity and AI makes headcount obsolete, what was all that dilution for?

And now comes the business model reckoning. SaaS companies built empires on per-seat pricing—predictable, high-margin, infinitely scalable. But AI forces a transition from selling seats to selling tokens. Suddenly these companies need to understand their cost of inference. What’s their gross margin on a token? Do they even know?

The SaaS category was always overpriced—stocks trading at 20-30x revenue on the promise of eventual profitability that never materialized. Now they’re being asked to rebuild their entire pricing model while figuring out inference economics on the fly. ServiceNow’s consumption-based “Flex Credits” and Salesforce’s ~$0.10/action pricing are early experiments, but no one knows yet whether these unit economics actually work at scale.

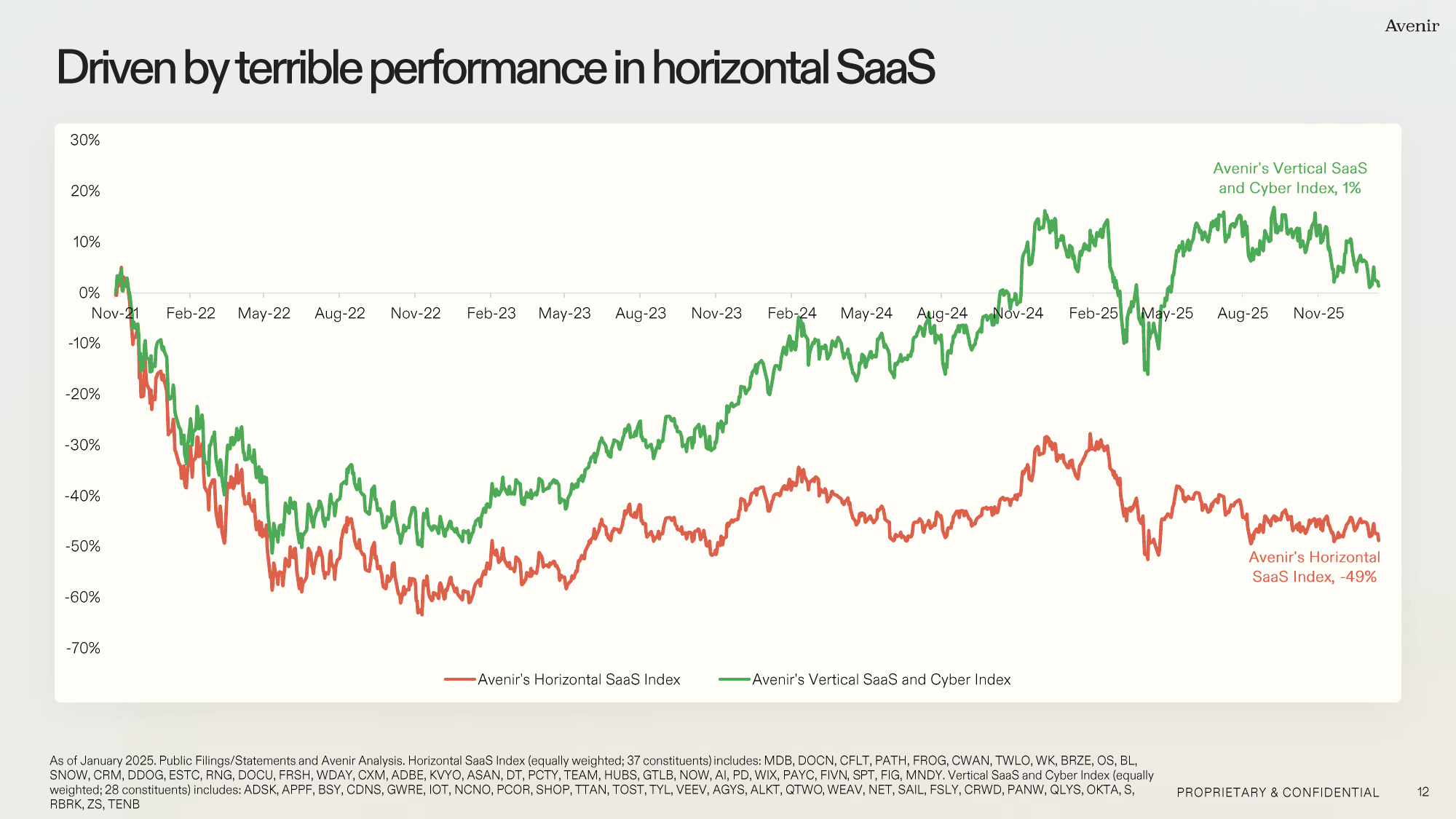

The Horizontal vs. Vertical Divergence

Not all SaaS is getting crushed equally. The market has already figured out what matters.

Source: Avenir analysis. Horizontal SaaS Index (37 constituents) vs. Vertical SaaS and Cyber Index (28 constituents). As of January 2026.

Horizontal SaaS—the Mondays, the Asanas, the generic workflow tools—is down 49% since November 2021. Vertical SaaS and cybersecurity is roughly flat. That’s a 50 percentage point divergence within the same sector.

The market is telling us something important: generic is vulnerable, specialized is defensible.

Why? Horizontal tools compete on UI and workflow—exactly what AI agents can generate on demand. Vertical SaaS companies have proprietary data, regulatory expertise, and industry-specific context that AI can’t replicate from first principles. A vibe-coded Monday clone might work. A vibe-coded Epic Systems replacement faces decades of healthcare compliance built into every data model.

The Three SaaS Archetypes

Building on this divergence, let me sharpen the framework for evaluating which companies are exposed.

Most Exposed: AI Wrappers and Horizontal Tools

Companies whose AI is essentially GPT + custom prompts + RAG, or whose core product is workflow automation that agents now generate natively.

The problem: Most AI features are thin wrappers around OpenAI or Anthropic APIs. The differentiation isn’t in the model—it’s in the integration, the UX, the workflow automation. That’s real value. But it’s not $100/seat/month of value when the underlying inference costs are collapsing.

DeepSeek’s API pricing is now approximately 90% cheaper than OpenAI’s comparable offerings. Customer service AI platforms like Zendesk AI and Freshdesk Freddy are essentially GPT wrappers with CRM integration. The core product—ticketing, routing, analytics—remains valuable, but the AI premium is vulnerable.

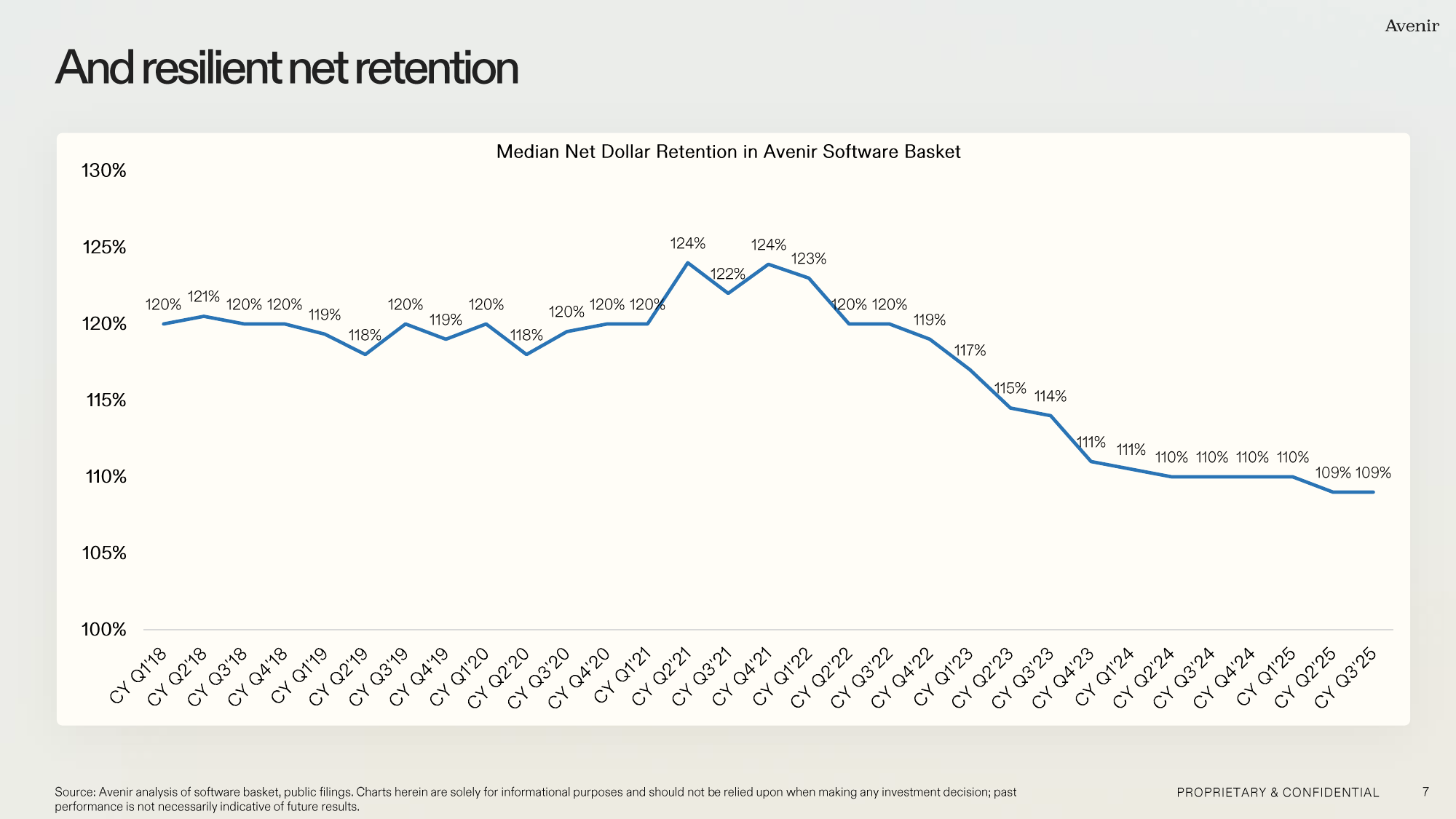

Defensible but Differentiated Value Declining: Workflow Lock-in

Salesforce owns your CRM data and processes. ServiceNow owns your IT workflows. That lock-in is real—but it’s separate from AI value.

The risk: Customers saying “I’ll keep your platform but skip your AI add-on.”

The Avenir data shows this fear is overblown—for now. Net dollar retention has declined from 120% in 2022 to 109% in Q3 2025, but that’s compression, not collapse. Customers are spending less incrementally, but they’re not leaving.

Source: Avenir analysis of software basket, public filings. As of Q3 2025.

The Winners: Vertical Depth and Infrastructure

Companies that provide the substrate for AI deployment rather than the AI itself, or that have deep vertical expertise AI can’t replicate.

This is why I’ve focused BEP Research on infrastructure rather than applications. In my Inference Stack Depth piece, I mapped how NVIDIA is acquiring entire layers of the AI infrastructure stack. The insight: Value concentrates at the bottleneck, and the bottleneck is infrastructure.

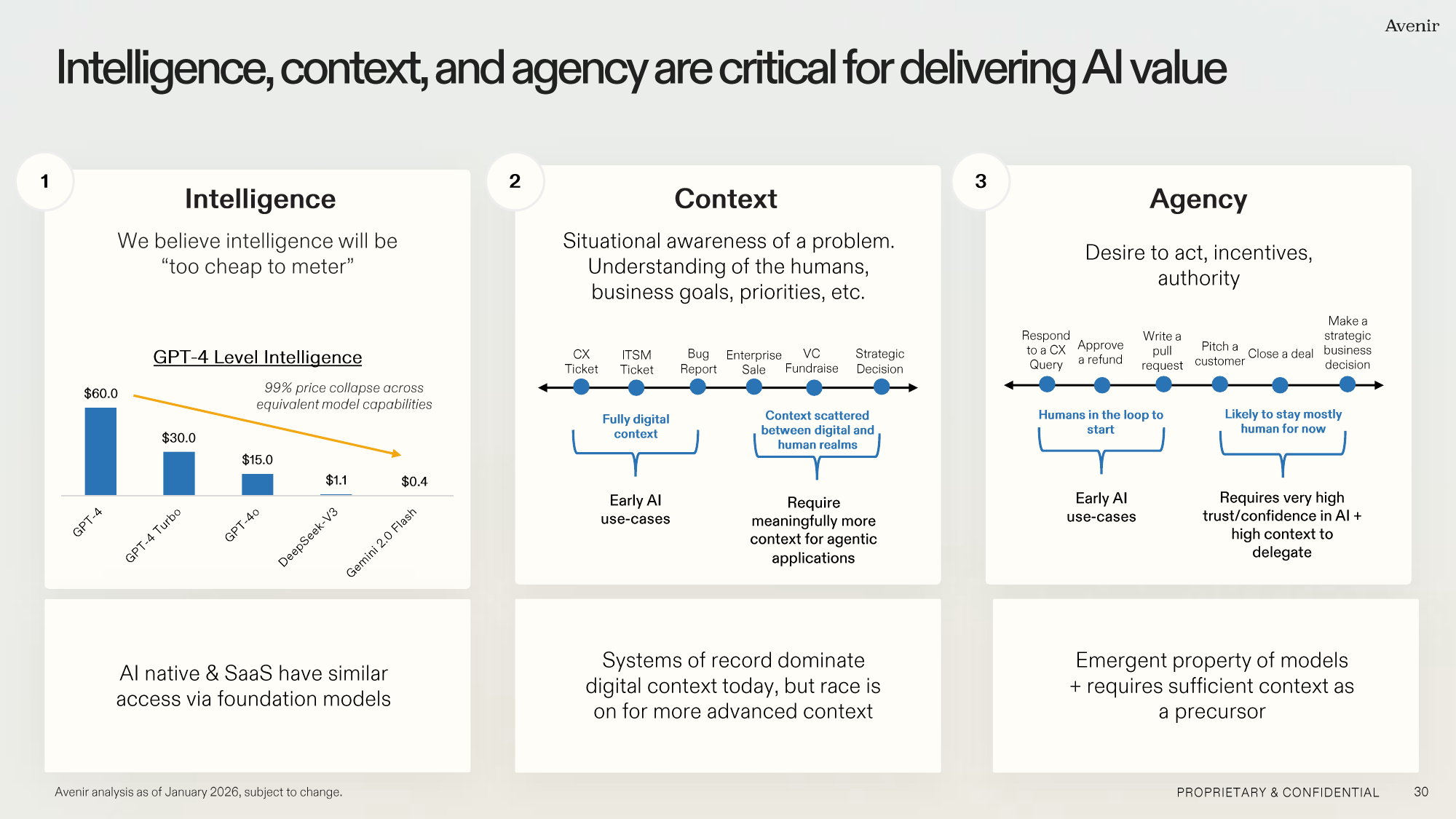

The Battle to Become a System of Context

Here’s where it gets interesting. Avenir’s January 2026 research introduces a framework that crystallizes what’s actually at stake.

They argue AI value creation requires three components: Intelligence, Context, and Agency.

Source: Avenir analysis, January 2026.

Intelligence is commoditizing rapidly. GPT-4 level capabilities have seen a 99% price collapse across equivalent models. Both AI-native startups and SaaS incumbents have similar access to foundation models. This layer is not where competitive advantage lives.

Context is the battleground. Situational awareness of a problem, understanding of humans involved, business goals, priorities. Systems of record dominate digital context today—your CRM knows your customers, your ERP knows your inventory, your HRIS knows your employees. But the race is on for more advanced context: cross-platform awareness, historical patterns, human judgment signals.

Agency—the ability to act autonomously—requires context as a precursor. You can’t delegate a task to an AI agent without giving it the context to execute. This is why systems of record are more valuable in an AI world, not less: they’re the context that makes agency possible.

The strategic implication: SaaS companies must evolve from “systems of record” to “systems of context.” They need to collect more data, more signals, more understanding of the humans and workflows they serve. The companies that can provide rich context to AI agents will capture the orchestration layer. Those that can’t will be reduced to dumb data stores.

This is a more nuanced picture than “SaaS is dead.” It’s “SaaS must evolve or die.”

What the Buyers Actually Think

The “SaaS is cooked” narrative on Twitter is compelling. But what do actual enterprise buyers think?

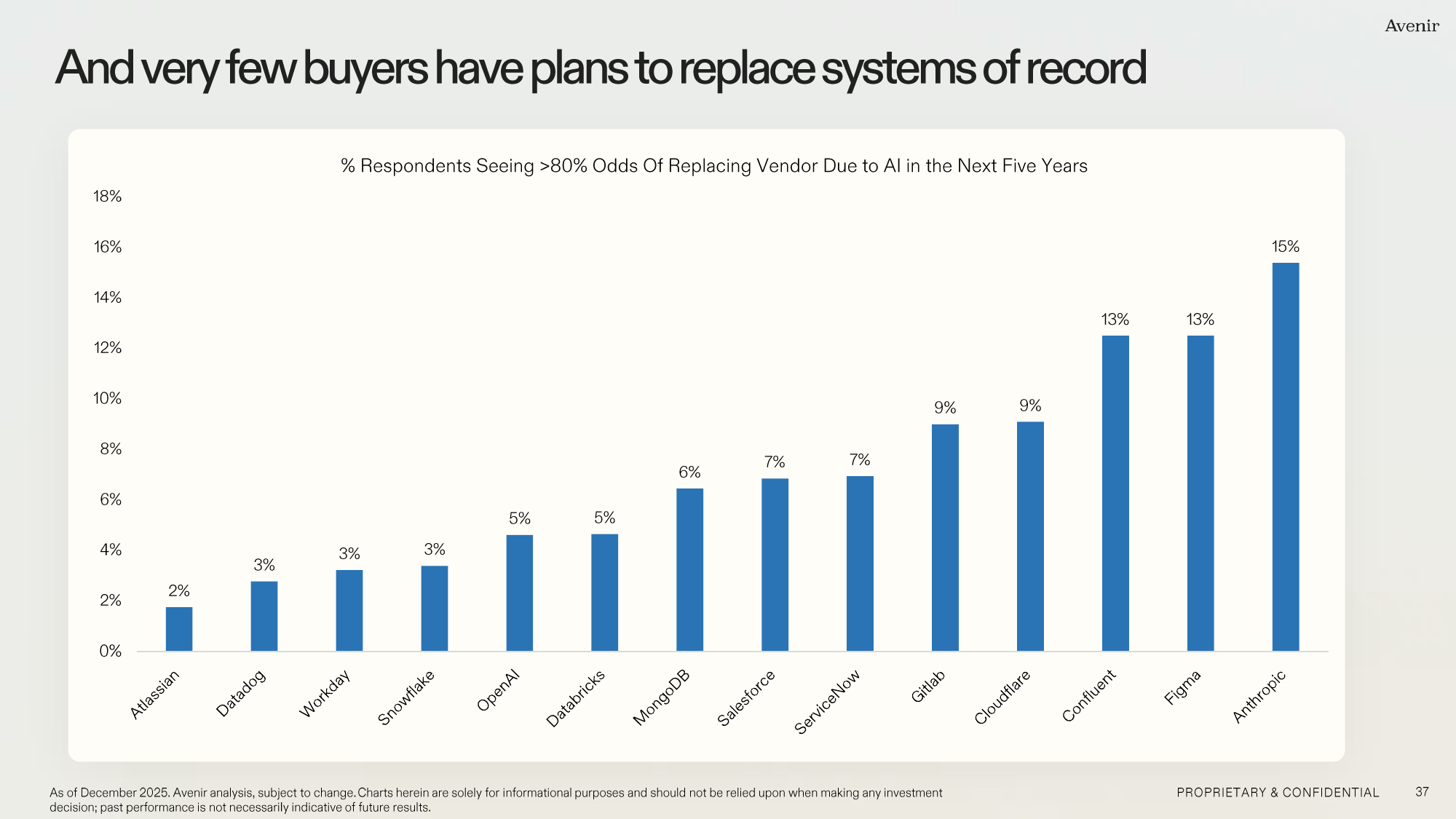

Avenir surveyed enterprise software buyers and found something surprising: only 8% believe their existing software vendors will be losers due to generative AI. 63% expect existing vendors to benefit.

Source: Avenir analysis, December 2025.

Even more telling: when asked about the probability of replacing specific vendors due to AI in the next five years, the numbers are remarkably low. Only 2% see >80% odds of replacing Atlassian. 3% for Workday. 6% for Salesforce. 7% for ServiceNow.

Enterprise software is sticky for reasons that have nothing to do with AI. Migration costs. Training. Integrations. Compliance requirements. The CIO who rips out Workday for a vibe-coded alternative is taking career risk that no one will reward them for.

David Sacks made this point on the All-In podcast this week: “The idea that you’re just going to rip out that system and replace it with code that’s been probabilistically generated by an AI engine yesterday with a small team to maintain it internally. This doesn’t seem realistic to me. So again, I think this very dire prediction of all SaaS is dead is overstated.”

But Sacks also identified the real vulnerability: “If you’re a SaaS product that charges a lot of money and people only use a handful of your features, then you are a target to be ripped out with something that’s more bespoke. Because the ROI just isn’t there.” The existential question isn’t replacement—it’s where future value capture goes. SaaS becomes an older layer, and users want to work across AI rather than within siloed applications.

This doesn’t mean SaaS is safe—it means the threat vector is different than the bears expect. It’s not replacement, it’s margin compression and seat-count reduction.

The Early AI Winners

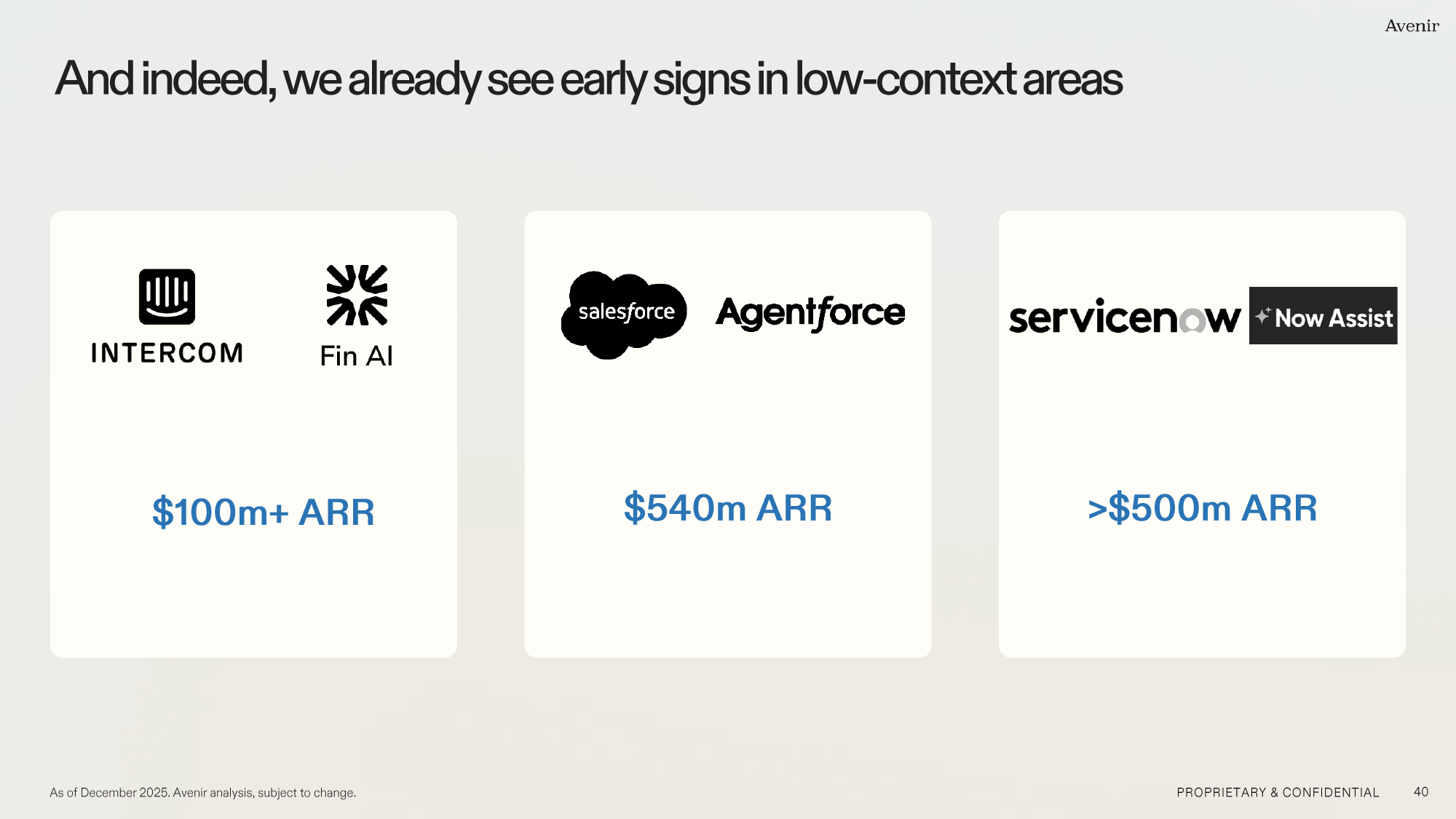

Meanwhile, SaaS incumbents are already generating real AI revenue—at scale.

Source: Avenir analysis, December 2025.

Salesforce’s Agentforce has reached $540 million ARR. ServiceNow’s Now Assist surpassed $600 million in net new ACV in Q4, exceeding expectations. Intercom’s Fin AI tops $100 million ARR.

These aren’t pilot programs. These are businesses at scale. McDermott is positioning ServiceNow as “the gateway” to enterprise AI—”the semantic layer that makes AI ubiquitous in the enterprise.” Whether that framing holds is the key question, but the revenue is real.

The incumbents have distribution, customer relationships, and the context data that AI agents need to be useful. AI-native startups have better models and faster iteration—but they’re building context from scratch while incumbents already have it.

The smartest incumbents are already adapting their business models. Salesforce’s Agentforce uses consumption-based “Flex Credits” rather than seats—approximately $0.10 per action. ServiceNow’s “Pro Plus” SKU commands a 30%+ premium to unlock AI capabilities. This is the transition from selling software-for-humans to selling infrastructure-for-agents.

The Data Quality Reality

Let me share a story from my own operating experience that illustrates why the “agents will replace enterprise software” thesis is more complicated than it appears.

At Deco Lighting, we ran on SAP Business One. In theory, it was our single source of truth—inventory, orders, financials, everything. In practice, if the data going into SAP wasn’t clean, nothing coming out was reliable. The system was only as good as the discipline we maintained in feeding it.

I tried multiple solutions to extract more intelligence from our data. We bought a HANA box—SAP’s in-memory platform marketed as the AI and analytics layer for exactly this purpose. It didn’t solve the underlying problem. We implemented Domo for business intelligence dashboards. The visualizations were beautiful, but the data still had to be massaged and reconciled before the cards meant anything.

You know what actually worked? Our CFO eventually pulled everything into Excel spreadsheets. He’s literally running the business through pivot tables now—not because Excel is superior technology, but because he could see the data, validate it, and trust it.

This is the dirty secret of enterprise software that the “AI will replace everything” narrative misses entirely. The bottleneck was never the interface or the analytics layer—it was data quality, data governance, and the institutional knowledge required to know when the numbers were wrong. Those problems don’t disappear when you add AI agents. They get worse.

When Karpathy describes agents making “subtle conceptual errors that a slightly sloppy, hasty junior dev might do,” he’s describing exactly this problem at the software layer. Agents don’t surface inconsistencies. They don’t push back when assumptions are wrong. They run confidently with bad data and produce plausible-looking outputs that fail in ways you won’t catch until something breaks downstream.

The Verification Problem

Here’s where my infrastructure focus connects back to Karpathy’s observations.

ServiceNow CEO Bill McDermott framed this perfectly on their Q4 2025 earnings call: “AI is probabilistic, which by definition means we can’t be certain about the results. Workflow orchestration is deterministic, predictable, no randomness, which is required given the sophistication and governance of running global enterprises. AI doesn’t replace enterprise orchestration. It depends on it.”

This is exactly right. Karpathy noted that agents work with “tenacity”—they never get tired, never get demoralized, just keep going. “It’s a ‘feel the AGI’ moment to watch it struggle with something for a long time just to come out victorious 30 minutes later.”

But he also warned that the models “definitely still make mistakes and if you have any code you actually care about I would watch them like a hawk.”

In coding, you have compilers and test suites that catch errors. In enterprise workflows, you have... what exactly?

This is the verification gap I’ve been writing about. When ServiceNow deploys thousands of AI agents across an enterprise—handling IT tickets, HR requests, customer service cases—who audits whether they’re making the “subtle conceptual errors” Karpathy describes?

The companies that solve verification and governance—not just generation—will capture the next wave of enterprise value. This is infrastructure, not application layer. It’s why I’m watching the orchestration and observability space more closely than the AI copilot space.

The LED Parallel

When I was building Deco Lighting, we watched LED commoditization happen in real-time. Early movers charged premium prices for “integrated solutions.” Within five years, the underlying technology became commodity, and the winners were companies with genuine differentiation in design, distribution, or customer relationships—not just “we were early to LEDs.”

The same pattern is playing out in AI, just faster.

DeepSeek demonstrated 90%+ cost reduction versus Western competitors in both training and inference. API pricing is deflating rapidly. The question for every SaaS investment: When AI inference costs approach zero, what’s actually left?

The Investment Framework

For those allocating capital in this environment, here’s how I’m thinking about it:

As Akram of The Razor’s Edge put it last week: “I will not ‘own’ a software business at over 10x revenue. Yes, I will trade some names for sure for little windows, but ownership land for me at this point is 5x revenue or lower.” That’s a useful heuristic. ServiceNow at 20x EV/sales last summer was priced for perfection. The compression was inevitable once the SaaS narrative turned.

Avoid: Paying “AI premium” multiples for companies whose AI is commodity inference with UX. The customer service AI platforms, the horizontal copilot add-ons, the AI-native startups built entirely on foundation model APIs. Watch Rule of 40 claims skeptically—demand GAAP profitability.

Watch carefully: Workflow lock-in companies like ServiceNow, Salesforce, Workday. The platform value is real. The AI premium value is uncertain. Monitor for the “keep your platform, skip your AI add-on” dynamic in enterprise renewals. The early AI ARR numbers are encouraging but the margin profile matters.

Consider: Vertical SaaS with proprietary training data in high-compliance verticals. Infrastructure plays like Databricks and Snowflake that benefit regardless of model winner. Companies solving bottlenecks in verification, governance, and orchestration. Companies making the transition from “system of record” to “system of context.”

Prefer: Companies solving bottlenecks. As I argued in The Packaging Paradox, the defining characteristic of 2026’s AI landscape is that constraints matter more than raw performance. Companies solving bottlenecks—in power, packaging, memory, verification—will outperform those dependent on bottleneck resolution.

Karpathy’s Warning for All of Us

Let me close with Karpathy’s most sobering observation: “I’ve already noticed that I am slowly starting to atrophy my ability to write code manually.”

Generation and discrimination are different capabilities. You can review code just fine even if you struggle to write it.

The same dynamic is coming for every knowledge work category. The professionals who maintain the ability to verify AI output—to catch the “subtle conceptual errors”—will command premium value. Those who become dependent on AI generation without maintaining discrimination skills face the same atrophy Karpathy describes.

For enterprise software companies, this suggests a different competitive axis entirely. The value isn’t in generating AI output—that’s becoming commodity. The value is in verifying AI output at scale. In governance. In accountability frameworks. In being the system of context that makes AI agents useful.

That’s infrastructure. And infrastructure is where the smart money is heading.

What I’m Watching

ServiceNow as AI's workflow operating system: McDermott's framing deserves a deeper look. If AI is probabilistic and workflow orchestration is deterministic, then ServiceNow becomes the governance layer that makes AI agents enterprise-safe. Open-source models plus NVIDIA infrastructure plus deterministic automation could be the legacy SaaS killer—or the platform that captures the orchestration premium. The question is who unlocks real pricing power from AI in 18 months. ServiceNow is well-positioned, but as Akram notes, it still needs a valuation carrot. Deep dive coming soon.

Enterprise renewal patterns: Are customers keeping platforms but dropping AI add-ons? NDR compression continues—will it stabilize?

The system of context race: Who’s collecting the data that makes AI agents useful?

Verification tooling: Who’s building the audit layer for agent swarms?

Vertical vs. horizontal divergence: Does the 50 percentage point gap widen further?

GAAP profitability: When do investors stop accepting the Rule of 40 bullshit?

If you found this analysis valuable, please share it—it helps more than you know. And if you haven’t subscribed yet, now’s the time. BEP Research will be moving to paid soon in the coming weeks. I’m committed to delivering institutional-quality analysis on AI infrastructure that you won’t find anywhere else.

Resources

Chamath Palihapitiya’s “Great SaaS Meltdown” thread on X (January 21, 2026)

The Razor’s Edge: Meta Magic & Narrative Netherlands (January 29, 2026)

The Verification Gap: Who Audits the Agent Swarm? - Part 3 of the Co-Design Series

NVIDIA’s Inference Stack Depth Strategy - Part 2 of the Co-Design Series

The Memory Wall: Why Groq and Jamba Had to Find Each Other - Part 1 of the Co-Design Series

The Packaging Paradox: Why CoWoS—Not 2nm—Is the Real AI Bottleneck

About the Author

Ben Pouladian is a Los Angeles-based tech investor and entrepreneur focused on AI infrastructure, semiconductors, and the power systems enabling the next generation of compute. He was co-founder of Deco Lighting (2005–2019), where he helped build one of the leading commercial LED lighting manufacturers in North America. Ben holds an electrical engineering degree from UC San Diego, where he worked in Professor Fainman’s ultrafast nanoscale optics lab on silicon photonics and micro-ring resonators, and interned at Cymer, the company that manufactures the EUV light sources for ASML’s lithography systems.

He currently serves as Chairman of the Leadership Board at Terasaki Institute for Biomedical Innovation and is a YPO member. His investment research focuses on AI datacenter infrastructure, GPU computing, and the semiconductor supply chain. Long-term NVIDIA investor since 2016.

Follow on Twitter/X: @benitoz | More at benpouladian.com

Disclosure: The author holds positions in NVIDIA and related semiconductor investments. This is not investment advice.