The Dirty Discount

The market repriced one company’s governance as a scandal and never touched the demand underneath it.

“…unwilling to be associated with the financial statements prepared by management.”

— Ernst & Young, resigning as the company’s auditor, disclosed in an October 30, 2024 filing.

That is close to the worst sentence an auditor can write about a client. Eighteen months later, the same company priced a seven-billion-dollar raise to buy the components for a thirty-nine-billion-dollar book of AI server orders. Both facts are true at the same time, and the distance between them is the whole opportunity. I am going to make you wait for the name, because the name is exactly what the market is using as an excuse not to look.

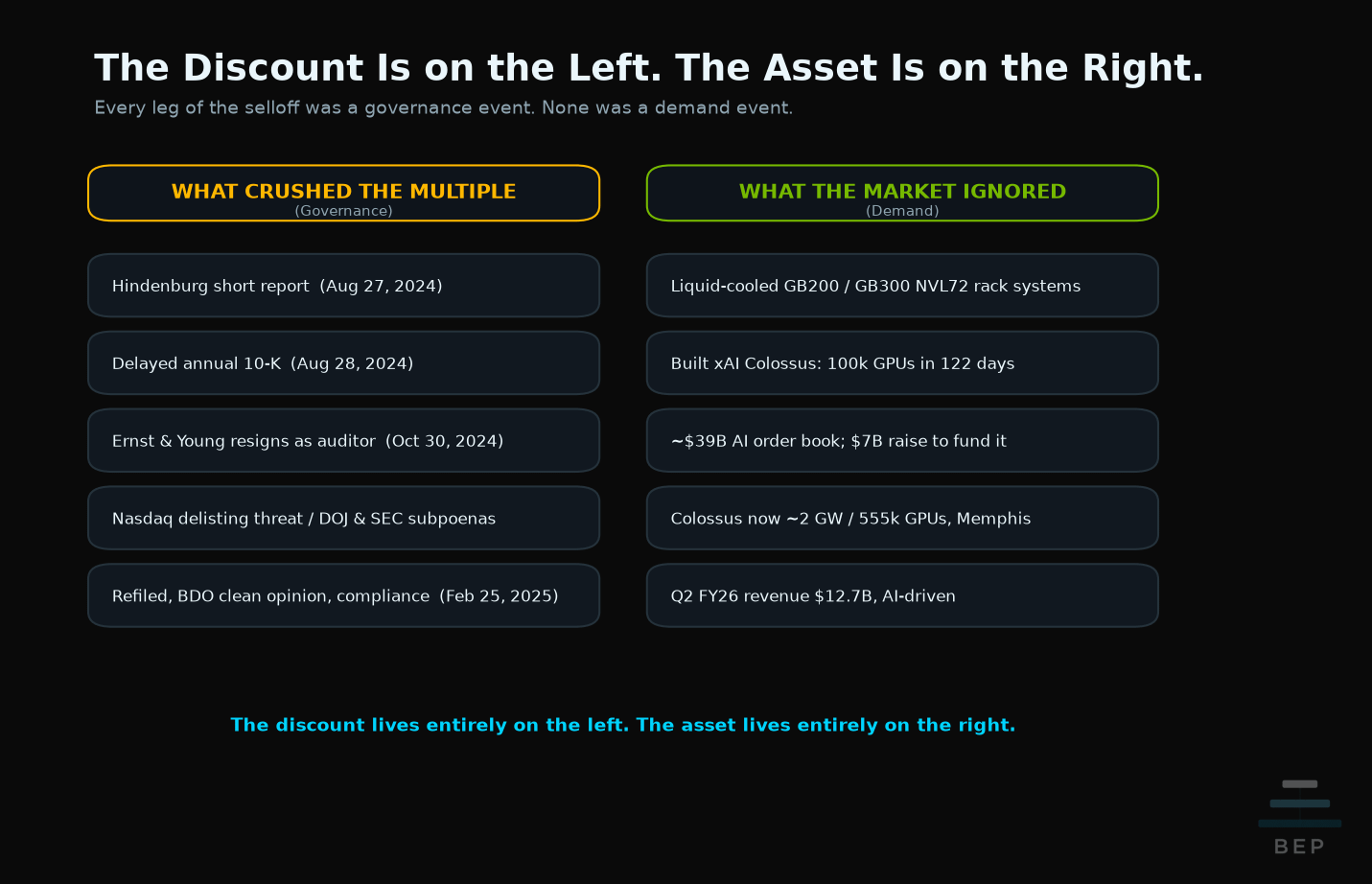

The market spent two years pricing this company as a governance problem: a delayed 10-K, a short report, an auditor resignation, a delisting clock, federal subpoenas, and this spring a co-founder arrested for conspiring to divert Nvidia servers to China. Each headline knocked the multiple down another leg, and even after the books were refiled the company that builds the racks for the most demanded compute on earth still trades like a distressed box-shifter.

The scandal repriced the governance. It never repriced the demand.

The Discount Came From the Books, Not the Backlog

Every leg of the selloff traces to a governance event, and not one of them touched a unit of demand. Walk the timeline. Ernst & Young flagged the audit committee in July 2024. Hindenburg published its short thesis on August 27. The company delayed its annual 10-K the next day, drew a Nasdaq non-compliance notice on September 20, and confirmed a Justice Department inquiry that same month. Ernst & Young resigned on October 30 and the stock fell roughly 30% in a session. A new auditor was engaged in November, a special committee reported no evidence of fraud or misconduct in December, and the company refiled its delinquent statements by the February 25, 2025 Nasdaq deadline and regained compliance. Every one of those is a real governance failure. None of them is a statement about whether hyperscalers and neoclouds want liquid-cooled rack-scale AI systems.

A company can be a governance mess and a demand monster at once, and the market hates that combination because it cannot underwrite it cleanly. So it discounts the whole enterprise to the level of its worst headline, and the name screens as broken while it ships into the tightest capacity market the data center has ever seen.

This is the inverse of the setup I described in The Quality of the Beat: Why Credo (CRDO) Beat, Raised, and Fell: “The market did not reprice the size of the beat. It repriced the quality of it.” Credo printed a clean beat and fell because the market repriced who the revenue came from and when the next leg arrived. This company is the mirror: the market repriced the integrity of the books and left the quality of the demand alone. Same machine, opposite stain.

The Asset Is the Cooling Loop, and It Just Became Mandatory

This company does not screen as an AI winner because the market still files it under “server assembler,” and that filing is two rack generations out of date. The thing it builds is no longer a box. It is a direct-liquid-cooling rack-scale system, and at the power densities Nvidia is shipping into, liquid cooling stopped being an option and became a physical requirement. This is the company that stood up the racks for xAI’s Colossus in Memphis — 100,000 Nvidia GPUs in 122 days on liquid-cooled systems — a cluster that has since grown past half a million GPUs across H100, H200, and Blackwell GB200 and GB300 parts. The cooling loop is the reason it could be built that fast.

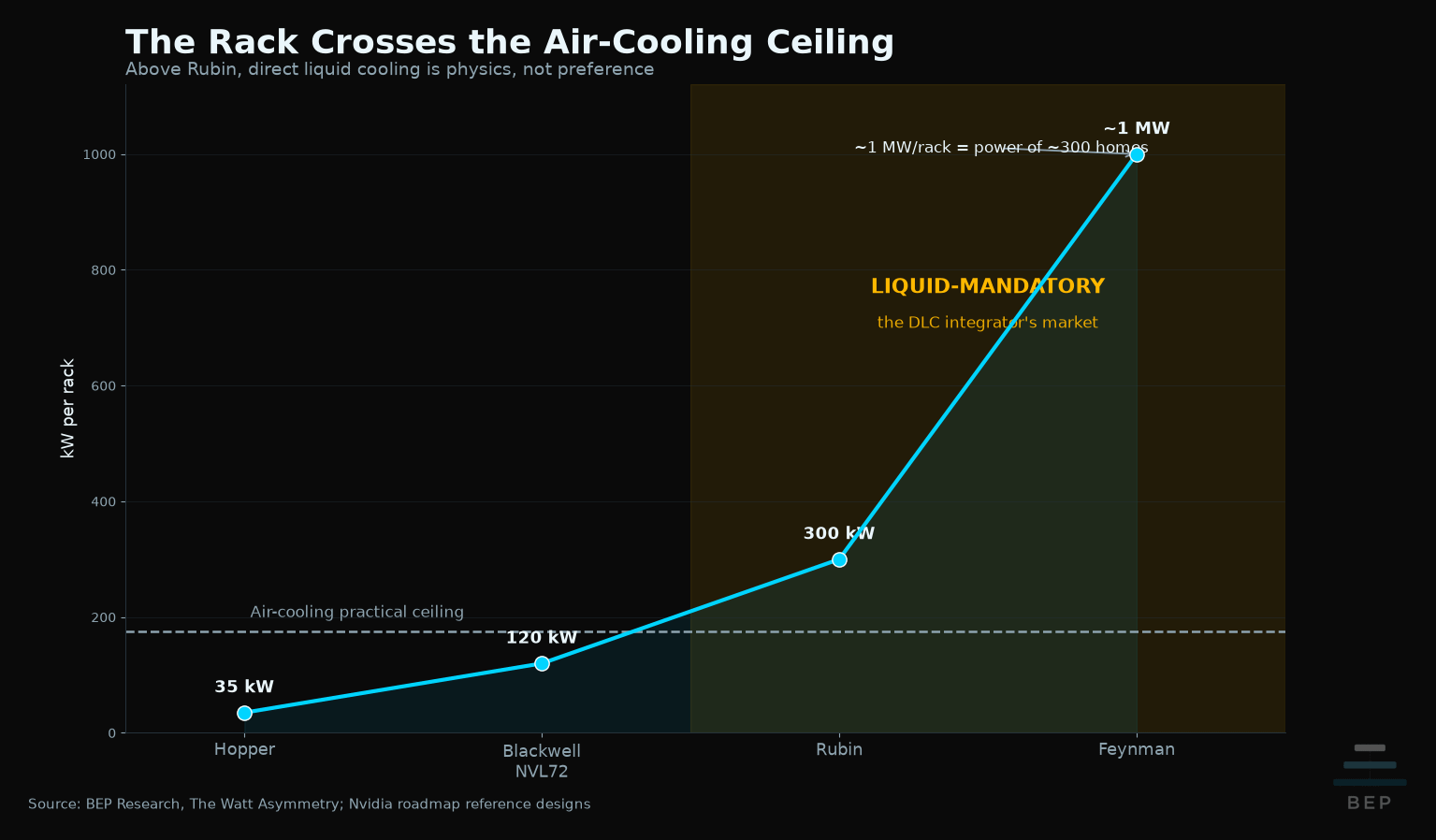

I laid out the mechanism in The Watt Asymmetry. Rack power density is on a three-year ramp from roughly 120 kilowatts at Blackwell NVL72 to 300 kilowatts at Rubin to a target near one megawatt per rack at Feynman. You cannot cool a megawatt with air. Above that threshold liquid cooling is the only path that works, which is why the integrators who can deliver it at rack scale move from commodity to chokepoint as the density curve climbs. This company is one of the named GB200 and GB300 NVL72 direct-liquid-cooling integrators in the Nvidia ecosystem, and it markets the loop on its own numbers: roughly 40% power savings and 98% heat capture per rack against air.

The market is pricing it for the margin profile of bending sheet metal. The asset it actually owns is the ability to deliver the cooling architecture every megawatt-class rack now requires, at the speed the buildout demands.

It Sits Inside the Financing Loop, Not Outside It

The reason the demand never wavered is that the rack integrator is the step where the money becomes a machine. In The Token Dollar, I argued the AI infrastructure economy runs one loop: borrow dollars, buy GPUs, mint tokens, sell tokens for dollars, service the carry, roll the principal, with the GPU fleet as collateral. The rack integrator is the step nobody models, the point where the borrowed dollars convert into the physical asset that backs the loan. Before a GPU mints a single token, somebody has to rack it, cool it, and power it. That somebody is the DLC integrator, and the June raise is exactly that conversion priced in the open.

The June 10 pricing term sheet spells it out: 45.45 million common shares plus 75 million depositary shares of a new 7.00% Series A mandatory convertible preferred, roughly $1.25 billion of common and $3.75 billion of convert, with up to $2 billion more available through an at-the-market program. The use of proceeds is not vague either; the filing states the money funds “the purchase of components to satisfy the approximately $39 billion of orders … from more than 20 customers” the company plans to fill in future quarters. A load-bearing node in a loop measured in the hundreds of billions, with its booked demand written into an SEC filing, still priced like a vendor that might lose its listing.

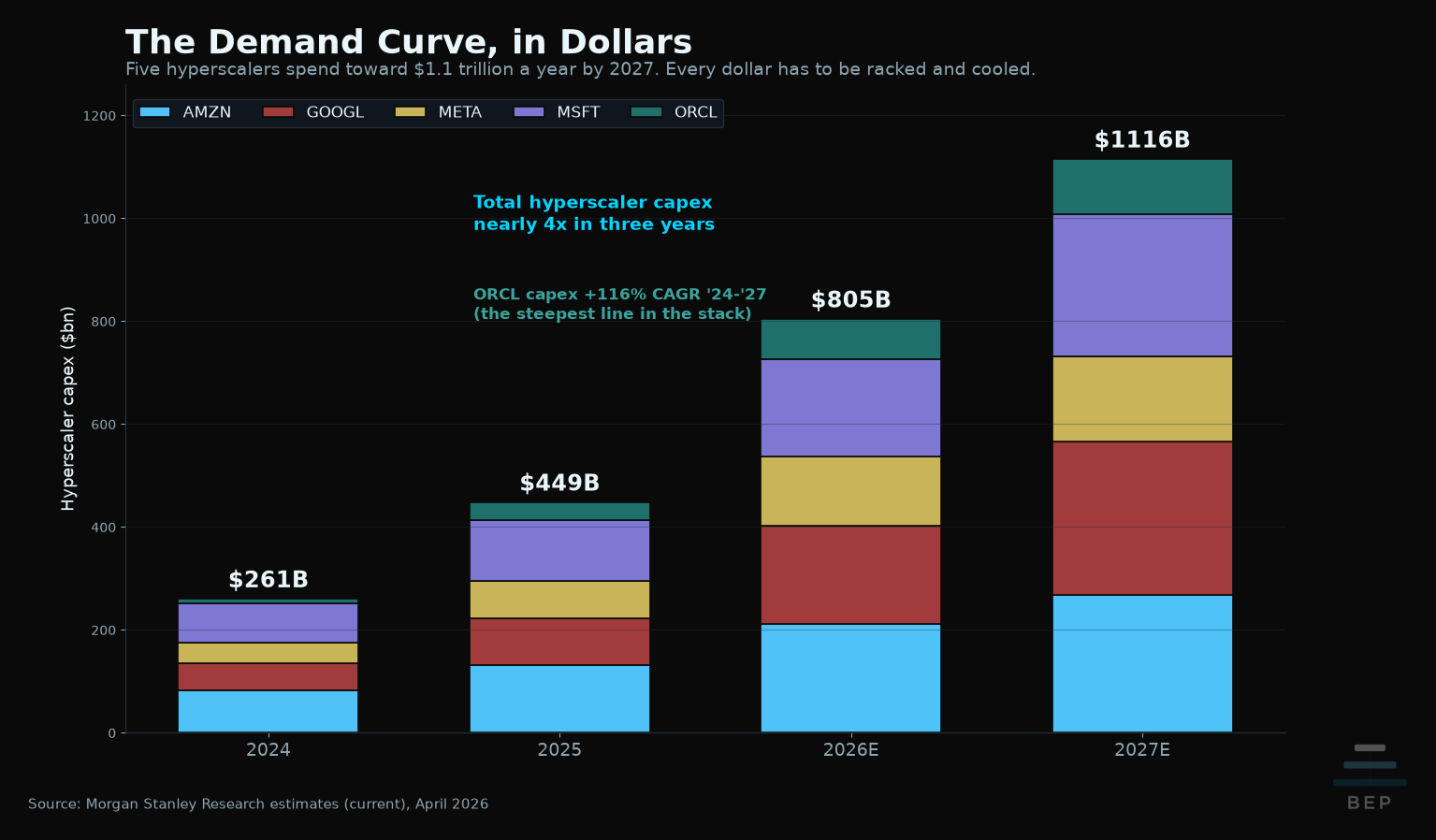

And the loop is still widening. Morgan Stanley now models the five largest hyperscalers spending roughly $805 billion of capex in 2026 and approaching $1.1 trillion in 2027, up from $765 billion and $950 billion only a quarter earlier, with Oracle’s line compounding at a 116% annual rate off the lowest base. That is the demand curve in dollars, and every one of those dollars has to be racked, cooled, and powered before it computes anything. The rack-and-cool layer is the toll booth the whole number passes through.

Here is the tell. Every other major name that builds these machines has been repriced for that demand this year. Dell, HPE, and Lenovo have all re-rated hard in 2026, each of them at least doubling on the year. One name on the same demand curve has done the opposite and fallen, and the only thing separating it from the rest is the stain on its books. That divergence is the entire trade, and I will name the company below.

xAI Is the Catalyst That Forces the House Clean

The clean-up will not happen because the board found discipline. It will happen because the demand got too large to leave stranded behind a governance cloud. xAI merged with SpaceX in February 2026 into a single entity valued near $1.25 trillion, the most valuable private company in the world, and that treasury now funds the Memphis Colossus build-out where this company is a direct-to-chip liquid-cooling partner. The campus already runs at two gigawatts across three buildings, and on our read the trajectory runs toward roughly 3.5 gigawatts as the SpaceX-funded phase comes on, underwritten by the combined balance sheet rather than by xAI’s own cash flow, which is still deeply negative. When a customer of that scale leans on a vendor, the governance overhang stops being the vendor’s problem alone and becomes a shared problem the supply chain has every interest in resolving fast.

And the balance sheet just got larger. SpaceX came public this month in a reported $75 billion raise, and the dollars behind that print are not really a bet on rockets. They are a bet on power: the gigawatts, the racks, and the cooling loops the model and its agent fleet consume. This is the live case of what I mapped in The $4 Trillion Scarcity Trade — private-market scarcity does not stay private, it becomes capex, and the capex lands on whoever builds the physical machine. The integrator that racks and cools those gigawatts is one of the names that premium has to pay. Today the buyer doubled down again, striking a $60 billion all-stock deal for Cursor, the AI coding agent, buying the demand layer that consumes the very compute these racks run. The money is not slowing; it is integrating vertically, from the agent down to the watt.

You can already see it routing through the system. Google is reportedly paying SpaceX on the order of $920 million a month for Blackwell capacity tied to xAI, the same scarcity marked at the cloud layer instead of the integrator layer. Every dollar of it runs through racks that have to be built and cooled, and the integrator captures a slice of each one. This is one of the cheapest ways to stand in that flow, precisely because the accounting cloud is still keeping institutional money on the sidelines.

And the vendor is not being shy about it. As the IPO priced, the company’s own CEO went on X to congratulate Musk on “SpaceX’s greatest IPO” and said he was “proud to co-build another new Gigawatt AI datacenter for SpaceX and xAI within a year,” calling it his fastest build yet. Read that as the supply side raising its hand in public. The integrator the market is still discounting for an accounting scandal is the one announcing a brand-new gigawatt cluster for the most aggressive compute buyer alive, four days before I wrote this.

Below the paywall: the name and the ticker, the CEO’s on-record line that put the catalyst on a one-year clock, the re-rating gap against the peer group that left this name behind and what it decomposes into, why Nvidia needs this house cleaned, the full bear case including the live China export-control indictment and the customer who holds the pricing whip, and where I stand on the name with sizing.