The Quiet Architect

Why Marvell Is Building the Nervous System of AI

Good morning to my West coast readers, sit down, pour yourself a nice cup of coffee. This past week may have been the most consequential seven days for AI optical interconnects since I started covering this space.

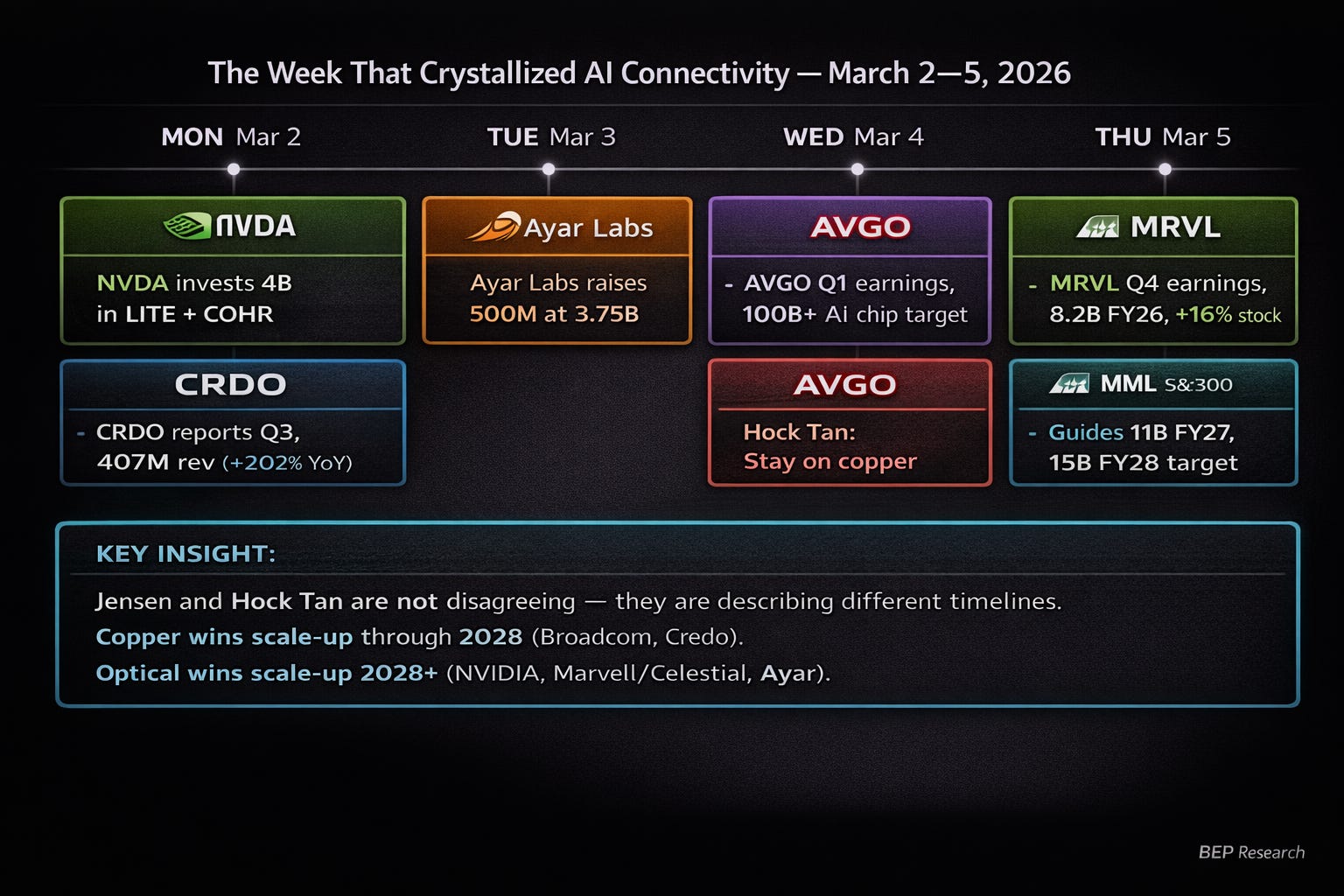

On Monday, NVIDIA invested $4 billion in Lumentum and Coherent, and Credo reported record Q3 earnings, tripling revenue year-over-year. On Tuesday, Ayar Labs raised $500 million at a $3.75 billion valuation. On Wednesday, Broadcom’s Hock Tan told the market that his customers want to stay on copper. And on Thursday, Marvell reported earnings that beat estimates, guided to $11 billion in FY2027 revenue, and watched its stock jump 16%.

Four days. Three earnings reports. A $4 billion photonics investment. A $500 million startup raise. A copper counterargument from the most powerful voice in custom silicon. And an earnings print from a company most people still can’t quite explain.

If you’re trying to understand what’s actually happening in AI data center connectivity, who’s winning, where the money is flowing, and what it means, this is the week that crystallized it.

For those who’ve been following my coverage, it validated several things I’ve been writing about for months. In my December Optical Interconnect Deep Dive, I concluded: “The optical interconnect transition in AI datacenters is not a question of if, but when and how fast. The physics constraints are immutable — copper simply cannot deliver the bandwidth required for next-generation AI clusters at acceptable power levels.” This week, Jensen put $4 billion behind that thesis. Hock Tan told you exactly when. And Marvell showed you what it looks like to be positioned on both sides of the transition, for better and worse.

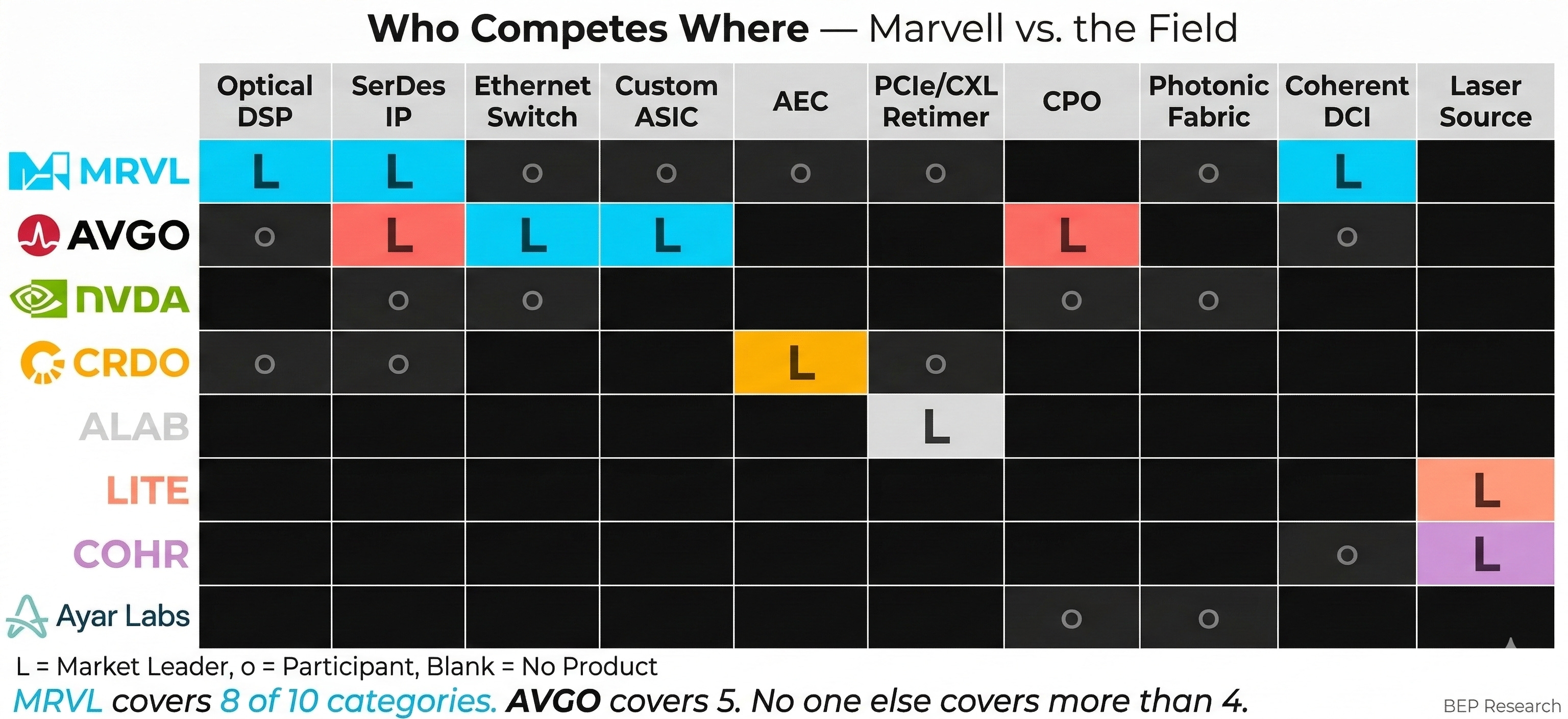

What Marvell Actually Is Now

Most people have heard the name but couldn’t tell you what Marvell does. Ten years ago, they made hard disk drive controllers. Storage chips. WiFi chips. Consumer electronics. That was the company.

Then Matt Murphy became CEO in 2016 and began one of the more underappreciated strategic pivots in semiconductor history. He wound down low-margin consumer businesses and made a series of acquisitions that, viewed in sequence, reveal a coherent architecture:

2018 — Cavium: Networking and ARM processor capabilities. Not a connectivity play, but a platform play. Cavium gave Marvell the engineering team and IP base to compete at data center scale.

2019 — Avera Semiconductor (from GlobalFoundries): This is the one most people miss. Semi-custom and full-custom ASIC design capability. Without this deal, Marvell has no custom silicon business. The custom business that just did $1.5 billion in FY2026 traces directly back here.

2021 — Inphi and Innovium: High-speed optical interconnect technology and cloud-optimized switching. Inphi made Marvell the dominant player in optical DSPs overnight.

December 2025 — Celestial AI ($3.25B, up to $5.5B with earnouts): Photonic Fabric, connecting chips with light. The largest optical interconnect acquisition of the AI era.

January 2026 — XConn Technologies (~$540M): CXL switching and the team developing UALink scale-up switches, the open-standard alternative to NVIDIA’s NVLink.

Murphy’s formula is consistent: buy the technology that will be essential in the next generation before anyone else is paying attention. Every acquisition filled a specific gap. None were headline-grabbing at the time. All look prescient now. But there’s a less generous read of this story: Marvell has spent over $15 billion on acquisitions in eight years because it couldn’t build these capabilities organically. Broadcom grew its CPO and SerDes franchises in-house. NVIDIA built its optical engines internally. Marvell bought its way into every layer. That works until it doesn’t. Integration risk is real, and the two most expensive acquisitions (Celestial AI and Inphi) are in businesses where Marvell had no prior presence.

The result is a company that went from $5.5 billion in revenue to $8.195 billion in two years, a 42% growth rate, with 74% of revenue now coming from AI data centers. On the earnings call, Murphy guided to $11 billion for FY2027, with quarterly revenue exceeding $3 billion by Q4. FY2028 is approaching $15 billion with non-GAAP EPS “well over $5.” His custom ASIC business alone scaled from zero to $1.5 billion in a single fiscal year.

The old image of a storage chip company is completely gone.

The Full-Distance Portfolio

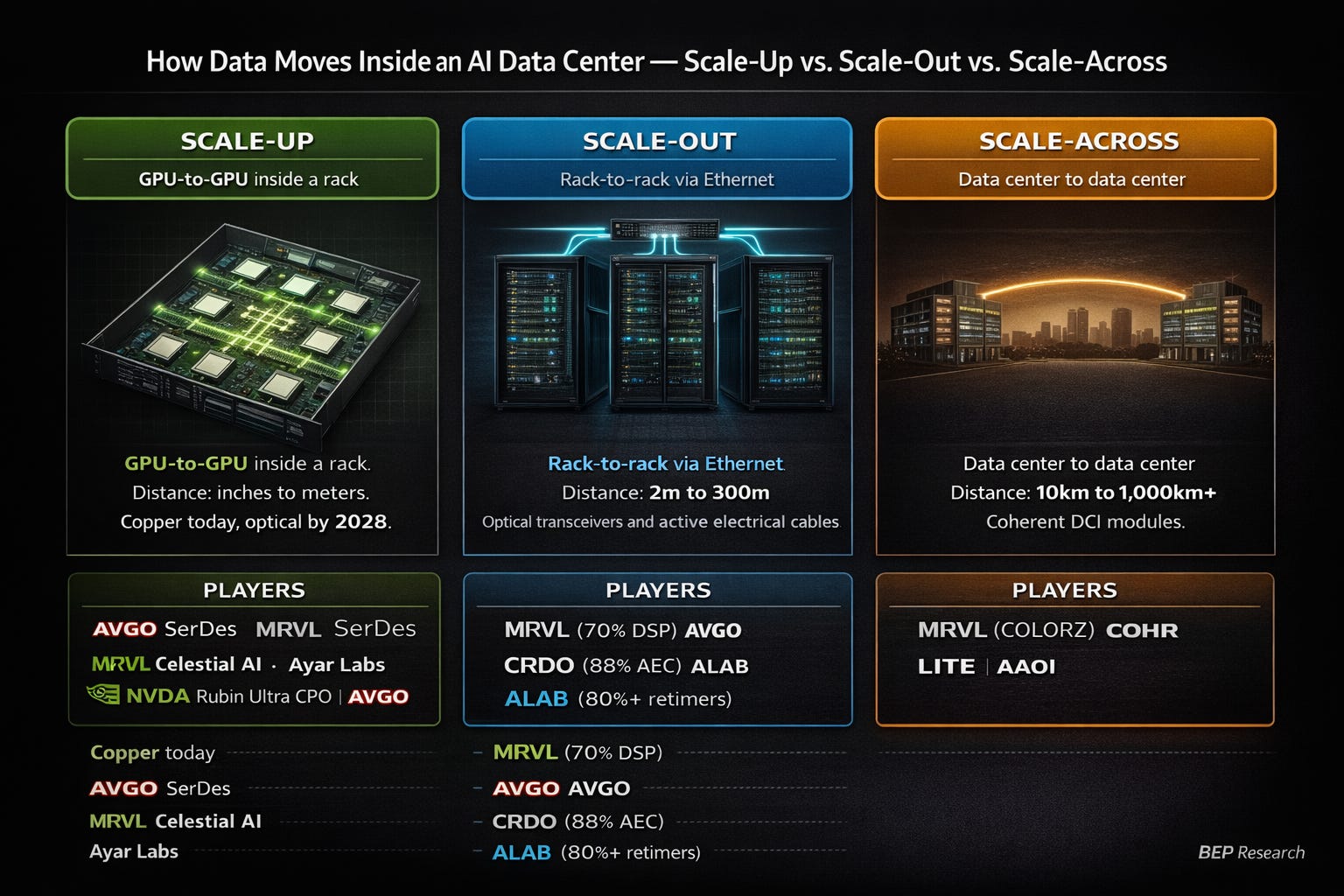

Here’s the framework that matters. It doesn’t matter how fast a GPU is if data can’t get to it on time. GPUs are the brain, but the nerves (interconnects) and blood vessels (memory channels) have to run without bottlenecks. What Marvell builds is exactly that.

AI data center connectivity breaks into three zones based on distance. Scale-Up covers GPU-to-GPU within a package or rack. Scale-Out covers rack-to-rack via Ethernet. Scale-Across covers data center to data center over fiber. Marvell now has technology across nearly all three, and that full-distance coverage is its most underappreciated advantage. It’s also, potentially, a sign of a company spread too thin. Covering every layer and leading none of them is a real risk.

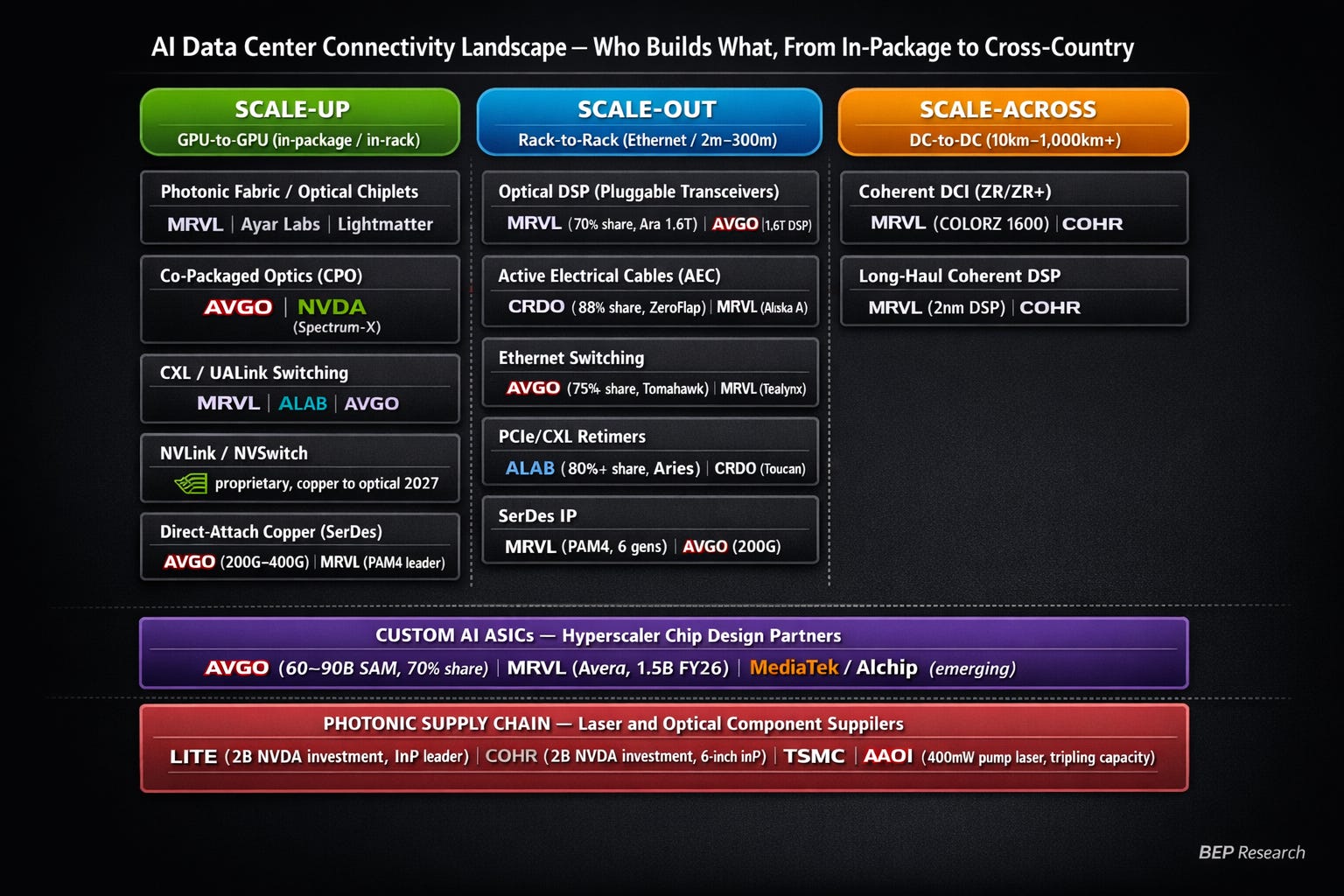

Optical DSPs. Inside an AI cluster, data travels as electrical signals between GPUs over short copper distances. Beyond a few meters, copper degrades. Optical cables take over, carrying light instead of electricity. The DSP inside each optical module does the hard part: modulating data onto light on the transmit side and recovering a weakened, distorted signal into clean data on the receive side. Using PAM4 modulation, a single light channel carries four amplitude levels simultaneously, and signal integrity at these speeds compounds nonlinearly as you move from 800G to 1.6T.

Marvell holds roughly 70% market share here. Its Ara DSP, built on 3nm and the industry’s first 1.6T product, cuts module power by more than 20%. By the time competitors catch up to 800G, Marvell is already shipping 1.6T. Murphy confirmed strong bookings from multiple Tier 1 customers, with 1.6T revenue expected to ramp rapidly in FY2027.

SerDes IP. Every high-speed chip in an AI data center (switch chips, custom ASICs, optical DSPs, memory controllers) contains SerDes (Serializer/Deserializer) IP that bundles parallel data into high-speed serial links. A single hyperscale rack contains tens of thousands of SerDes links. Marvell pioneered PAM4 modulation for SerDes ten years ago and has maintained leadership through six generations.

The investment insight: when a hyperscaler designs their own AI chip using Marvell’s SerDes, switching vendors in the next generation requires a full chip redesign from scratch. That switching cost is Marvell’s hidden moat, and it ties the SerDes business to the custom ASIC business in a self-reinforcing loop.

CPO and Photonic Fabric. Co-Packaged Optics pulls the optical module inside the chip package itself, shortening the distance electrical signals travel. Marvell has talked about its 3D SiPho Engine CPO technology for years, but to be blunt, there’s no public demo, no published performance data, and no confirmed production shipments. The Celestial AI acquisition looks less like a complement and more like a replacement. Celestial’s Photonic Fabric stacks optical chiplets directly on top of chip dies in 3D. The OMIB (Optical Multi-Die Interconnect Bridge) connects multiple large dies optically within the package. The vision is to bind thousands of GPUs optically into a single massive computer and disaggregate memory into a unified pool of 33TB+. Revenue begins late FY2028, ramping to $1 billion annually by end of FY2029. AWS has already signed a warrant agreement.

The honest read: Marvell’s CPO story before Celestial AI was thin. The $5.5 billion acquisition was the admission that they needed real photonic technology, not just a roadmap. Whether Celestial delivers is now the bet.

Active Electrical Cables. For the 2-9 meter distances inside racks, too far for passive copper but too close for optical, AECs fill the gap with an integrated DSP chip that amplifies and corrects the signal. Marvell’s Alaska A DSP powers these cables, and its Golden Cable initiative provides cable vendors with validated designs as a platform. Foxconn shipped its first product using Golden Cable in two months. Murphy expects combined AEC and retimer revenue to more than double year-over-year in FY2027.

CXL switching. As AI models scale, there isn’t enough memory to attach to a single GPU. CXL (Compute Express Link) is a protocol built on top of PCIe that allows memory disaggregation, so server A can use idle memory from server B. Through XConn, Marvell gained CXL switching capability plus UALink development for open-standard scale-up connectivity. Combined with its earlier Tanzanite CXL memory controller acquisition, Marvell has the most comprehensive portfolio in disaggregated memory connectivity. If AI inference is memory-bound, not compute-bound, and I’ve argued repeatedly that it is, then the company building the pipes to move memory data faster is building the right thing.

Coherent DCI. For long-haul distances, tens to thousands of kilometers between data centers, Marvell’s COLORZ modules plug directly into switches, cutting costs up to 75% versus traditional appliances. Alongside earnings, Marvell announced COLORZ 1600, the industry’s first 1.6T coherent pluggable. Murphy confirmed Marvell expects to supply DCI modules to all five major U.S. hyperscalers this year.

Custom ASICs. AWS Trainium. Microsoft Maia. Hyperscalers design their own AI chips to reduce NVIDIA dependency, and Marvell does a significant portion of that design work. This capability was built on the 2019 Avera acquisition. Custom revenue doubled in FY2026 to $1.5 billion. Murphy expects 20%+ growth in FY2027 and at least a doubling in FY2028. The company has 50+ projects in progress with 10+ customers.

I want to be direct about where I stand on this business: I’m skeptical that custom ASICs have durable customer gravity. Marvell is a design-services partner, not a platform owner. There’s nothing preventing a hyperscaler from taking their next-generation chip to MediaTek, Alchip, or any other ASIC house that can offer competitive SerDes and packaging at a lower price point. The switching costs are real at the SerDes IP level (changing vendors does require a full redesign), but the design-services relationship itself is a contract, not a moat. Broadcom has stronger lock-in because it controls the entire XPU architecture. Marvell is closer to a high-end contractor.

The $1.5 billion in custom revenue is impressive execution. But I wouldn’t build an investment thesis around it doubling again without asking: what happens when the hyperscaler’s internal team gets good enough, or when a hungrier competitor underbids the next program? Murphy’s answer on the earnings call, “deeply engaged with the top four US hyperscalers,” is reassuring in the near term. It doesn’t answer the structural question.

What makes Marvell’s custom business more defensible than a standalone ASIC house is the interconnect portfolio wrapped around it. A hyperscaler using Marvell’s SerDes IP in their custom chip is likely also buying Marvell’s optical DSPs, switching silicon, and eventually CPO. Each layer reinforces the others. Strip out the custom ASICs, and Marvell still has the broadest connectivity portfolio in semiconductors. That’s the real asset.

Monday: Jensen’s $4 Billion Photonics Bet, and Credo’s Record Quarter

On March 2, NVIDIA announced $2 billion investments in both Lumentum and Coherent. Multiyear strategic agreements. Multibillion-dollar purchase commitments. Future capacity access rights for advanced laser components. Both companies will use the capital to build out U.S.-based manufacturing, and Lumentum CEO Michael Hurlston confirmed plans for a new fabrication facility.

This is Jensen putting $4 billion on the table to say: photonics is not optional for the next generation of AI infrastructure.

NVIDIA is adopting CPO for its Spectrum-X and Quantum-X photonic switches. The Rubin Ultra platform integrates optical scale-up at the GPU architecture level. Jensen needs the lasers, the silicon photonics, and the optical engines, and he’s willing to pay for guaranteed supply to get them. Every CPO switch, every coherent transceiver, every optical engine needs indium phosphide laser sources. Lumentum and Coherent are the two companies that can provide them at scale.

In The Great Photonic Divergence, published four days before this investment was announced, I wrote: “The laser shortage is the new CoWoS bottleneck — and the companies that own their own indium phosphide fabs will set the pace of the 1.6T transition.” Jensen apparently agrees. He just committed $4 billion to solving that exact bottleneck.

And it’s not just the big two. In that same piece, I detailed how Applied Optoelectronics ($AAOI), a roughly $4 billion market cap company that fabricates its own InP laser chips, reported that customer demand for laser sources exceeds what they can physically manufacture. They’re tripling fab capacity at their Sugar Land, Texas facility, with 95% of production dedicated to AI-specific lasers by year-end 2026. Their 400mW narrow-linewidth DFB pump laser positions them as a potential alternative supplier for CPO external laser sources, in the same supply chain lane that Lumentum occupies. When even the smaller players are supply-constrained and tripling capacity, the bottleneck isn’t a narrative. It’s structural.

The same day, Credo reported Q3 earnings that confirmed the other side of the connectivity thesis. Record revenue of $407 million, up 52% sequentially and more than 200% year-over-year. Non-GAAP EPS of $1.07, crushing the $0.94 consensus. Q4 guidance of $425-435 million. CEO Bill Brennan described it as the “most accelerated growth phase” in Credo’s history, with the company on track to triple revenue in FY2026.

I covered the full Q3 call in detail, but the headline for this piece is what Brennan said about copper vs. optical on the same morning Jensen invested $4 billion in photonics. He referenced NVIDIA directly: “I think they’ve been really outspoken that where you can use copper, you will use copper.” Then laid out why AECs win over laser-based optics at short distances: “Reliability. Number one. Power efficiency number two. And ultimately total cost of ownership.” Credo’s ZeroFlap AECs deliver 1,000x better reliability than commodity laser-based optics at half the power.

For Marvell, the NVIDIA/Lumentum/Coherent deals are a double-edged signal. They validate the photonic interconnect thesis that Marvell bet $5.5 billion on with Celestial AI. But they also show that NVIDIA is building its own optical supply chain, vertically integrated from GPUs through NVSwitch through optical engines through the laser sources themselves. That’s the kind of stack depth that makes competing at the platform level very difficult. And Credo’s results confirm that the copper-side business, where Marvell also competes via AECs and SerDes, is growing explosively right now, not in the future.

Tuesday: Ayar Labs and the Scale-Up Race

The day after NVIDIA’s photonics investments, Ayar Labs closed a $500 million Series E at a $3.75 billion valuation. Led by Neuberger Berman, with NVIDIA, AMD, MediaTek, Alchip, ARK Invest, and the Qatar Investment Authority participating. Total funding: $870 million.

Ayar is arguably the most advanced optical chiplet company in the private market. Its TeraPHY optical engines, built on TSMC’s COUPE silicon photonics process, can support over 200 Tbps of aggregate bandwidth per package, roughly 5x more than what NVIDIA’s Rubin GPUs deliver via NVLink. The company is working with GUC and Alchip on reference designs and recently opened a Hsinchu, Taiwan office to be closer to the TSMC packaging ecosystem.

The investor roster tells you who believes CPO is moving from lab to fab. NVIDIA is an existing investor doubling down. AMD is hedging alongside its Enosemi acquisition. ARK Invest brings growth conviction. And a sovereign wealth fund brings institutional validation. When QIA puts capital into an optical chiplet startup, the signal is clear.

This makes Ayar a direct competitor to Marvell’s Celestial AI Photonic Fabric for the scale-up optical opportunity. Both are targeting thousands of GPUs connected optically. Both are working with TSMC on packaging. The question is whether Marvell’s integration advantage (owning the full stack from DSPs to Photonic Fabric) outweighs Ayar’s focus advantage in doing one thing at industry-leading bandwidth density. We’ll likely know by 2028.

Wednesday: Hock Tan Makes the Case for Copper

In a week where $4.5 billion flowed into photonics, Broadcom’s CEO went the other direction.

On the Q1 earnings call, Hock Tan made an unequivocal argument for scale-up connectivity: direct-attach copper is the lowest latency, lowest power, and lowest cost way to connect XPUs within a cluster. Broadcom’s 200G SerDes, stepping up to 400G in 2028, can keep customers on copper for scale-up through at least 2028. His framing: the alternative of going to optical for scale-up “is more expensive and requires significantly more power.”

He was careful to note optical is fine for scale-out. But for GPU-to-GPU within a rack, Broadcom’s message was clear: stay on copper.

The market reaction was immediate. Corning dropped. Lumentum and Coherent, which had surged on the NVIDIA investment news two days earlier, gave back 4-5%. Credo, which makes the active electrical cables that extend copper’s reach, rallied nearly 10%.

This confirmed something I wrote in my Credo analysis a month earlier: “Copper is getting smarter, not dying. Credo’s AEC dominance proves that active copper solutions are displacing optics at short distances while optical wins at longer ranges.” Hock Tan just said the same thing on a call that moved $100 billion in market cap.

But here’s the nuance the market missed: Tan and Jensen are not disagreeing. They’re describing different timelines for different distances.

Broadcom’s copper argument is specifically about scale-up within racks through 2028. NVIDIA’s $4 billion photonics bet is about scale-up beyond 2027: the Rubin Ultra CPO integration, the infrastructure needed to get there, and the supply chain that has to be locked in years in advance. Corning’s own CFO confirmed on their January call that they see optical scale-up inflecting in 2028, exactly aligned with both Tan’s timeline and Jensen’s investment horizon.

They’re not arguing about whether optical wins. They’re arguing about when.

Friday postscript: As I was finishing this piece, S&P Dow Jones Indices announced that both Lumentum and Coherent will join the S&P 500 effective March 23. Four days after Jensen invested $4 billion in both companies, they get added to the most widely tracked index in the world. That’s not a coincidence. These were mid-cap optics companies 18 months ago. Now they’re S&P 500 constituents. If you needed one more signal that photonic infrastructure has moved from niche to core, this is it.

Thursday: Marvell Reports, and the Full Picture Comes Into Focus

Against this backdrop, Marvell’s Q4 report landed. $2.219 billion in quarterly revenue, beating guidance. $0.80 non-GAAP EPS, above the $0.79 consensus. Record full-year revenue of $8.195 billion. The stock jumped 16%.

Five things from the call that matter beyond the headline numbers:

Custom ASIC concerns are real, but may be priced in. Murphy said Marvell is deeply engaged with the top four US hyperscalers, with design wins at an all-time record. The near-term numbers look strong. I laid out my structural concerns in the portfolio section above. The long-term question about customer gravity remains unresolved, but the anxiety around near-term program losses may be overdone.

Switching is inflecting. Data center switching revenue exceeded $300M in FY2026 and is guided to surpass $600M in FY2027, up from the $500M expectation provided just last quarter. A 100T switching platform begins sampling in H1. This is Marvell’s most direct competition with Broadcom’s Tomahawk franchise. But let’s be honest about the gap: Broadcom has 75%+ market share and is already shipping Tomahawk 6 at 100 Tbps. Marvell’s Teralynx is a distant second. Doubling from $300M to $600M sounds impressive until you realize Broadcom’s networking revenue grew 60% year-over-year to billions.

The 1.6T transition is Marvell’s to lose. First-to-market with the 3nm Ara DSP. Strong bookings from multiple Tier 1 customers. The 800G-to-1.6T transition is where Marvell’s decade of PAM4 leadership compounds. Every generation of signal processing is harder, and learning curve advantages widen.

Celestial AI and XConn are in integration mode. Joint product roadmap discussions with customers are underway. Revenue contribution starts FY2028, but the strategic positioning matters now. These acquisitions fill the scale-up gap that was Marvell’s biggest portfolio weakness.

FY2028 is the real story. $15 billion in revenue. Non-GAAP EPS “well over $5.” Custom ASICs doubling. Celestial AI ramping to $1B. If Murphy delivers, the current valuation looks very different. But that’s a lot of “ifs” stacked on top of each other: a custom ASIC business with no structural lock-in has to double, a pre-revenue photonic acquisition has to hit $1B on schedule, and the optical DSP franchise has to hold 70% share through a generation transition where Broadcom is also claiming 1.6T leadership. Any one of those can slip.

The practical implication of this week’s confluence: Marvell is one of the few companies with products on both sides of the copper-to-optical transition. Its AEC and SerDes businesses benefit from copper extending its reign in the near term, exactly what Hock Tan described. Its Celestial AI Photonic Fabric positions it for the optical transition when it arrives, exactly what Jensen is investing billions to prepare for. Marvell doesn’t have to pick a side.

The Competitive Map

Marvell is not the only player here, and intellectual honesty requires acknowledging where the pressure is real.

Broadcom ($AVGO) is the most formidable competitor. Three generations of CPO shipping. TH6-Davisson at 102.4 Tbps sampling to hyperscalers. More than 75% Ethernet switch market share. An estimated $60-90B serviceable addressable market in custom AI accelerators, and Hock Tan said he has “line of sight” to AI chip revenue exceeding $100 billion in 2027. Broadcom’s vertical integration from switch ASICs to optical engines gives it a stack-depth advantage that Marvell’s Teralynx switching portfolio cannot yet match. And Tan’s copper argument buys Broadcom’s SerDes franchise at least two more years of runway before optical eats into it.

NVIDIA is vertically integrated from GPUs through NVSwitch to optical engines, and just invested $4 billion to lock in its photonic supply chain through Lumentum and Coherent. The Rubin Ultra CPO integration I covered at CES represents the scale-up inflection for 2027. When Jensen builds optical scale-up into the GPU architecture itself and simultaneously secures the photonic supply chain through direct investment, that’s a competitive moat pure connectivity companies struggle to match.

Ayar Labs is the private-market wildcard. At $3.75B valuation with NVIDIA, AMD, and sovereign wealth fund backing, Ayar’s TeraPHY chiplets compete directly with Marvell’s Celestial AI Photonic Fabric. Both target thousands of GPUs connected optically. Both work with TSMC on packaging. Integration advantage versus focus advantage: that competition will play out over the next three years.

Credo ($CRDO) owns 88% of the AEC market, the exact mid-distance zone where Marvell is pushing its Alaska A DSP and Golden Cable platform. As I detailed in my Q3 analysis, Brennan confirmed AEC adoption is still early even after a record quarter, and Credo is expanding into optical DSPs and ZeroFlap optics. The competitive overlap with Marvell is widening, not narrowing.

Marvell’s differentiation is breadth, not dominance at any single layer. No one else offers optical DSPs, SerDes IP, custom ASIC design, CXL switching, CPO, Photonic Fabric, AEC, and coherent DCI from a single vendor. Whether that breadth translates to sustainable competitive advantage or just complexity risk is the central investment question.

So What? — Why This Actually Matters

I want to be clear about my positioning: I don’t hold Marvell and I wasn’t a buyer on the earnings print. The 16% move didn’t change that.

Here’s why. Murphy has built something genuinely unusual, assembled through a decade of disciplined M&A. The interconnect businesses are strong: 70% optical DSP share, PAM4 SerDes leadership, and the Celestial AI acquisition filling the scale-up gap. If I were evaluating Marvell purely on its connectivity franchise, this would be one of the more compelling infrastructure stories in semis.

But the crown jewel revenue line, the $1.5 billion custom ASIC business that’s supposed to double again in FY2028, is the part that gives me pause. I detailed my concerns in the portfolio section: no platform lock-in, no guarantee the next design cycle stays with Marvell. When that business represents a growing share of the forward growth narrative, the structural risk matters.

The bull case is that the custom ASIC business is the Trojan horse that pulls in optical DSPs, switching silicon, and eventually CPO. The interconnect portfolio wraps around the custom chips and creates a bundled relationship that’s harder to unbundle than any single contract. That may prove right. But it’s a thesis, not a fact.

What I am confident about is the connectivity framework this week validated. The memory wall problem, the argument that AI inference is memory-bound, not compute-bound, is ultimately a connectivity problem at scale. The companies building the pipes to move data faster are building the right things. Whether Marvell’s assembled-through-acquisition approach can compete with Broadcom’s organic integration and NVIDIA’s vertical ownership is the question that will define its next chapter.

For the broader semiconductor ecosystem, Marvell’s full-distance coverage means it touches nearly every company in the AI connectivity stack as partner, supplier, and competitor simultaneously. Lumentum and Coherent supply lasers that go into Marvell’s optical modules, and AAOI is tripling InP laser capacity to try to keep up with the same demand. Credo and Astera Labs compete in AECs and retimers. Broadcom competes in switching and custom ASICs. NVIDIA competes on photonic platforms. The overlap creates both opportunities and complexity for portfolio construction.

I’m adding Marvell to the active coverage universe, not as a position, but because the connectivity infrastructure story now demands it. This week made that clear.

There's also a foundry layer underneath all of this that most investors haven't identified yet. The silicon photonics chips inside every optical engine, every 1.6T transceiver, every CPO module have to be fabricated somewhere. That story is coming next, for paid subscribers.

BEP Research Is Going Paid — and GTC Is Coming

This is my last free article.

I know there are a lot of Substacks out there. Some too technical, some too financial, most somewhere in between. What I try to do is different. I look at investing like systems. I try to see the forest through the trees. I won’t bombard you with spreadsheets or model outputs. I’m a long-term investor, not a trader. I don’t chase quarters or try to time earnings. My philosophy is to understand how the pieces connect, silicon to software to business model to investment thesis, and explain it in a way that helps you think, not just react.

That approach has served me well over the past 20 years. By writing my ideas here, it keeps me accountable.

BEP Research is going paid on March 9. Annual subscriptions are $400/year, but through March 9 you can lock in the early-bird rate of $350/year. Once the paywall goes up, the discount goes away. If you’ve been reading for free and finding value, now is the time.

GTC 2026 starts March 16. I’ll be there in person. On-site analysis of NVIDIA’s architecture announcements, networking roadmaps, and co-packaged optics developments will be a cornerstone of paid subscriber coverage.

Sources and Further Reading

About the Author

Ben Pouladian is a Los Angeles-based tech investor and entrepreneur focused on AI infrastructure, semiconductors, and the power systems enabling the next generation of compute. He was co-founder of Deco Lighting (2005–2019), where he helped build one of the leading commercial LED lighting manufacturers in North America. Ben holds an electrical engineering degree from UC San Diego, where he worked in Professor Fainman’s ultrafast nanoscale optics lab on silicon photonics and micro-ring resonators, and interned at Cymer, the company that manufactures the EUV light sources for ASML’s lithography systems.

He currently serves as Chairman of the Leadership Board at Terasaki Institute for Biomedical Innovation and is a YPO member. His investment research focuses on AI datacenter infrastructure, GPU computing, and the semiconductor supply chain. Long-term NVIDIA investor since 2016.

Follow on Twitter/X: @benitoz | More at benpouladian.com

Disclosure: The author holds positions in NVIDIA and related semiconductor investments. The author does not hold a position in Marvell ($MRVL). This is not investment advice. All investment decisions and their consequences are solely the responsibility of the reader.

I would dispute that marvell has better serdes than nvda.

The packaging and interconnect layer is where the real forward visibility sits right now. Ben's point about Marvell holding ~70% optical DSP share while simultaneously straddling both sides of the copper-to-optical transition is the exact dynamic that makes basket construction in this theme non-trivial. The Broadcom earnings comment about copper running to 2028 via SerDes, while Jensen simultaneously commits $4B to photonic supply chain, doesn't contradict, it confirms that the transition is a phased, layered migration where different parts of the value chain move at different speeds. The Celestial AI acquisition feels less like strategic clarity and more like a $5.5B admission that Marvell's organic photonics story was thin, but the 1.6T Ara DSP franchise on 3nm is hard to replicate. Does the breadth play (full-distance coverage) ultimately outcompete Broadcom's depth play (vertical ownership from switch to optical engine), or does being everywhere mean defending nothing?