How Credo (CRDO) Gives Zero Flaps!

Zero-Flap is Credo’s highest-ASP product, and a bet that reliability now caps how big an AI cluster can get. Reliability is the constraint.

Two quick notes. This explainer is free. BEP Research just crossed 3,000 subscribers, and I’m marking the milestone by taking it out from behind the paywall. I also built an interactive version so you can watch a single link flap stall a GPU cluster in real time. If it’s useful, a share is the best thanks.

What a “Flap” Actually Is, in Plain English

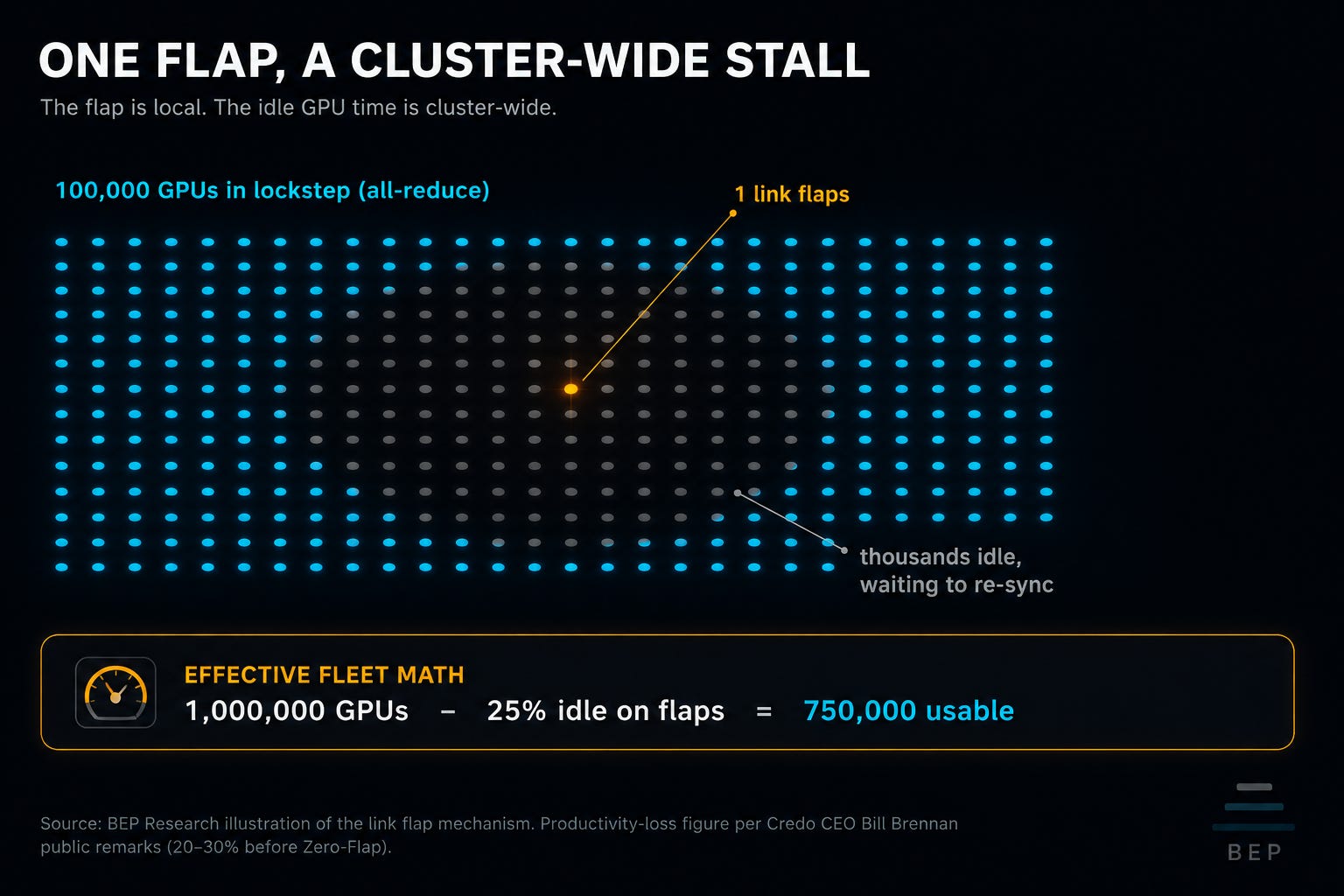

A “link flap” is a network connection that keeps dropping and reconnecting. On a laptop, it is the flaky Wi-Fi blip that makes a video call freeze for a second. Annoying, not catastrophic. The reason it matters for AI is that an AI training cluster is the opposite of a laptop: it is one hundred thousand GPUs that all have to stay in perfect lockstep.

Here is the mechanism, and it is the whole piece in one paragraph. Training a large model means the GPUs repeatedly do a synchronized step called an all-reduce, where every chip shares its partial result with every other chip and waits for everyone before moving on. It is a group operation. One slow runner stalls the entire group. So when a single optical link between two switches flaps, even for a moment, the GPUs that depend on that link fall out of sync, the collective operation stalls or restarts, and thousands of otherwise-healthy GPUs sit idle waiting. The flap is local. The damage is cluster-wide.

Now scale that to the part that makes it an investment story rather than an engineering footnote. The component most likely to flap is the laser inside a commodity optical module, also called a transceiver, the part that turns electrical signals into light and back. Lasers are the least reliable, most thermally sensitive, most failure-prone element in the link. As clusters grow toward gigawatt-class power draw and the link count per cluster explodes, the math gets ugly fast: more links, each with a small flap probability, means more flaps per hour, which means more idle GPU time. Credo CEO Bill Brennan has said publicly that one customer was losing 20 to 30 percent of its productivity to link flaps before deploying the Zero-Flap approach. At hyperscale, that is the gap between the fleet a customer paid for and the fleet it can actually use. Reliability here is not a feature. It is the limiting factor on usable compute.

This is the same point I made when Credo first preannounced its blowout quarter. As I wrote in Credo Just Proved the Optical Thesis: “One hyperscaler came to Credo because they were losing 20–30% of their uptime fighting optical link flaps.” That was framed then as a copper-versus-optics story. The Zero-Flap optical line is the same reliability philosophy, pushed out to the optical distances where copper physically cannot reach.

▶ See it in motion: I built an interactive simulation. Toggle commodity vs Zero-Flap optics and watch a single link flap stall the cluster and idle the GPUs in real time. tools.bepresearch.com/zero-flap

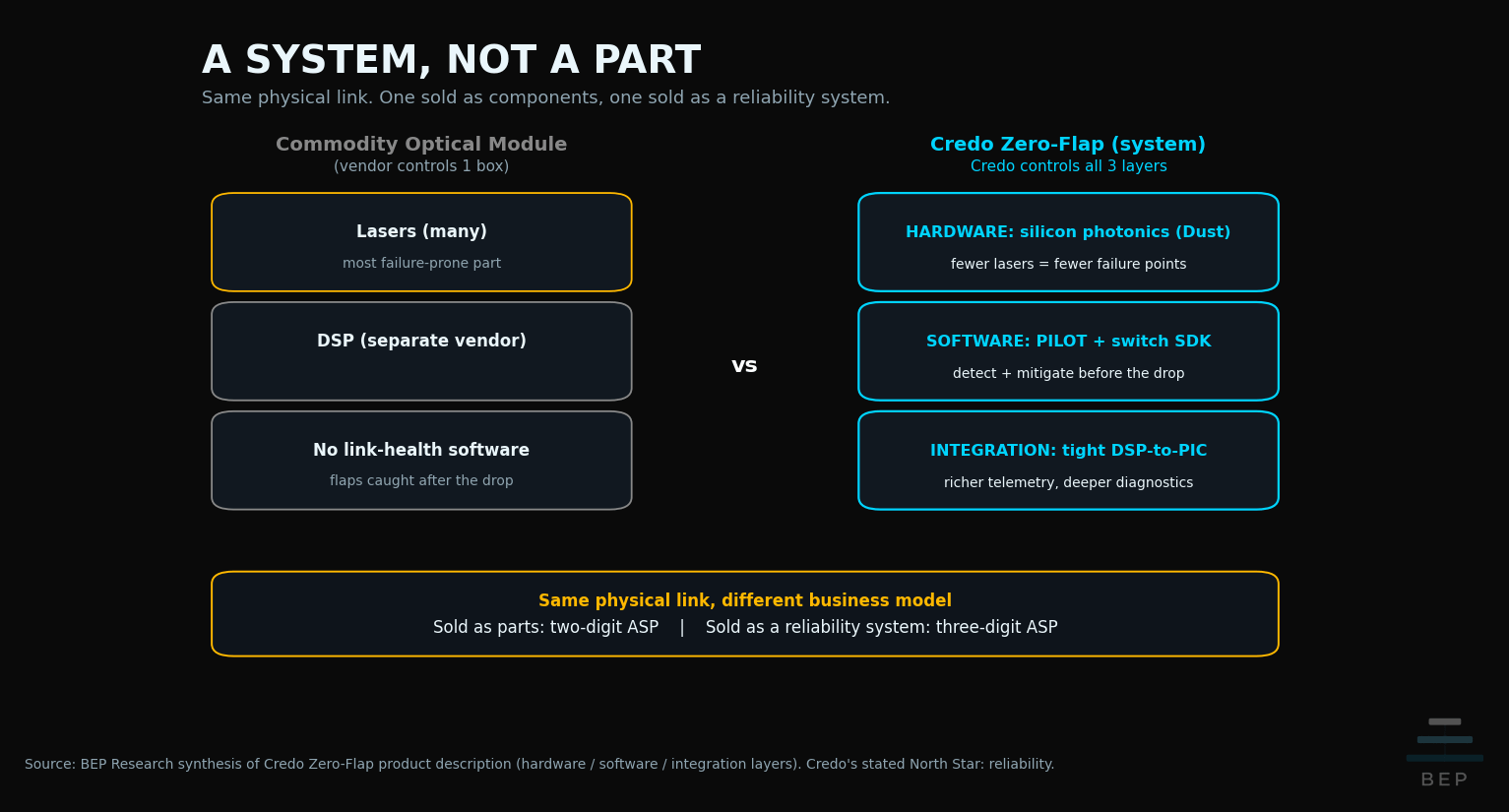

How Zero-Flap Works: Three Layers, One North Star

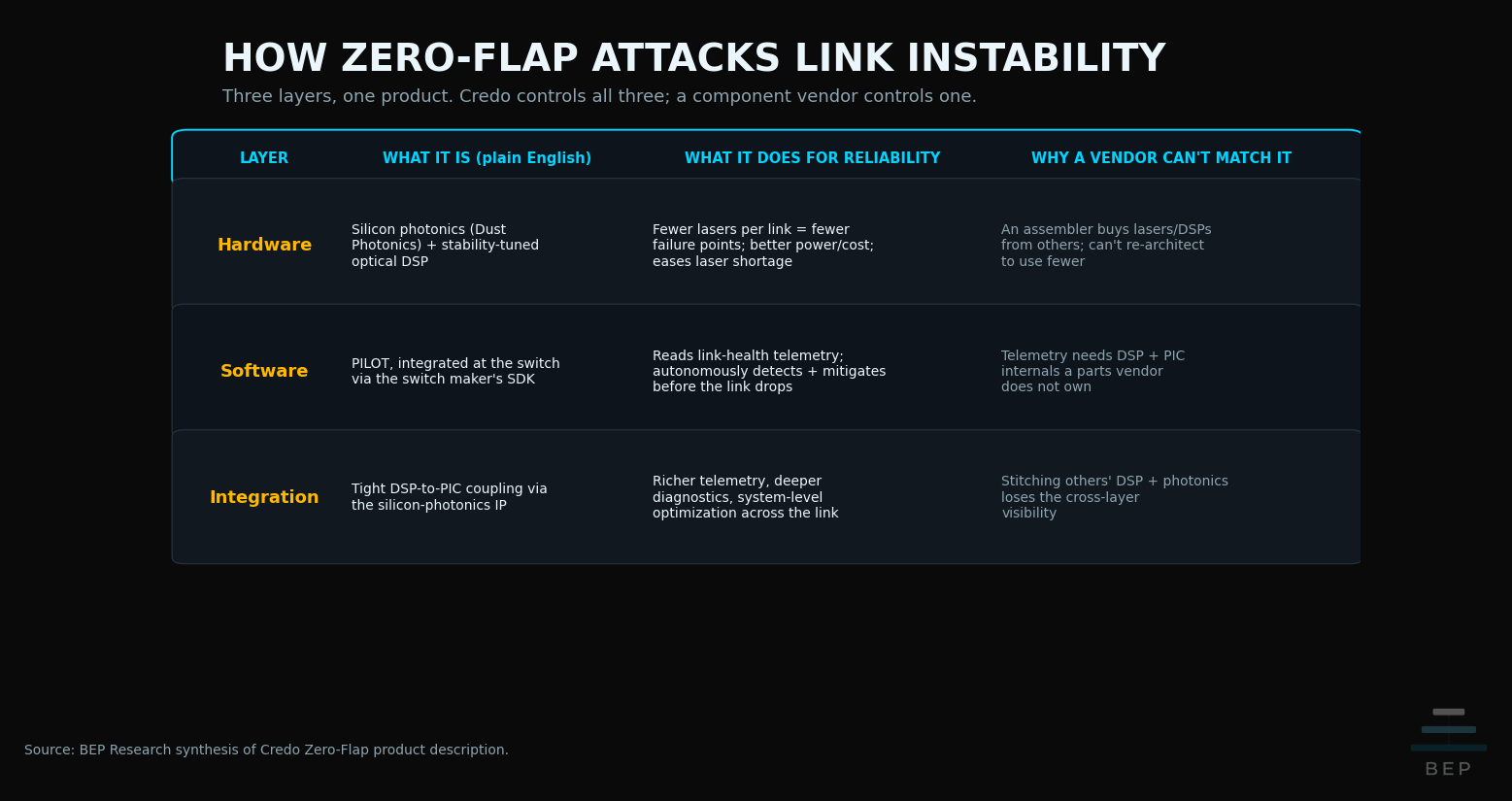

Zero-Flap attacks instability on three layers at once, which is exactly why Credo calls it a system and not a component. Start with what every optical link has to do: convert an electrical signal to light using a laser, push it down a glass fiber, and convert it back using a photodetector, with a digital signal processor (DSP, the chip that cleans up and reconstructs the signal) on each end. Every one of those steps is a place a link can degrade. Zero-Flap engineers against degradation at all three of the layers it can control.

1. Hardware: fewer lasers, fewer failure points. Through the Dust Photonics acquisition, Credo brings in silicon photonics, an approach that integrates much of the optical function onto a silicon chip and uses substantially fewer lasers per link. Fewer lasers means fewer of the single most failure-prone parts, better power and cost per link, and less exposure to the industry-wide laser supply shortage. Paired with an optical DSP tuned specifically for link stability rather than raw throughput, the hardware is built to flap less in the first place.

2. Software: catch the flap before it happens. Credo’s “PILOT” software, integrated at the switch level through the switch maker’s software development kit (SDK), continuously reads link-health telemetry, the bit error rates, signal-quality histograms, and laser-degradation signals coming off each module. Think of it as the check-engine light for the optical link: it reads the signals that precede a failure and autonomously detects and mitigates an instability condition before the link actually drops the cluster. Prevention, not cleanup.

3. Integration: own more of the stack, see more of the link. Because Credo controls both the DSP and, through the silicon-photonics intellectual property, the photonic integrated circuit (PIC, the chip where the light is generated and routed), it gets tighter DSP-to-PIC integration than a vendor selling one piece. Tighter integration means richer telemetry, deeper diagnostics, and system-level optimization that a component supplier stitching together someone else’s parts simply cannot match.

The result management claims is meaningful improvement in network reliability, faster time to a stable cluster, and longer uptime. This is the same mechanism I flagged the day the Q3 call landed. As I wrote in Credo’s Q3 Call Answered Every Question, what makes Zero-Flap a moat is the system integration delivering “autonomous detection and mitigation of link flap events before they impact the cluster.” The defensible part of a system like this is the hardware integration beneath it, far more than any single component, and that distinction is what the bear case below turns on.

Why It Matters Commercially: Three-Digit ASPs Change the Mix

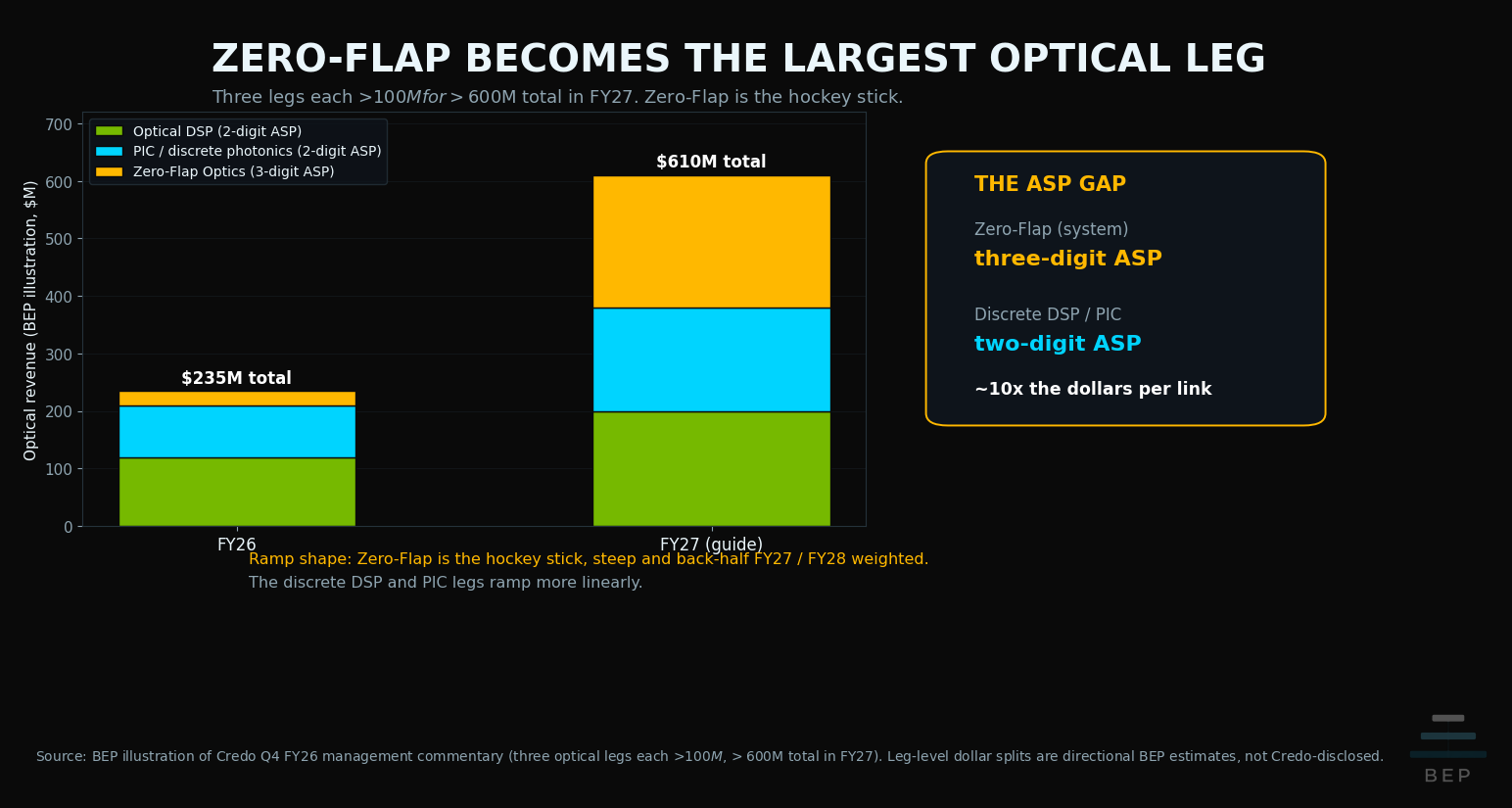

The reason Zero-Flap is the highest-leverage part of the Credo story is that it sells a system, not a part, and systems capture more dollars per link. On the Q4 FY26 call, Credo’s CFO framed the economics plainly in Q&A: Zero-Flap optics carries three-digit average selling prices (ASPs), versus two-digit ASPs for the discrete building blocks, the standalone optical DSP and the photonic integrated circuit. The same physical link, sold as an engineered reliability solution instead of a bag of components, captures roughly an order of magnitude more revenue. That is the whole commercial argument in one ratio.

Stack that ASP onto the volume story and you get management’s own math: as Zero-Flap ramps, it becomes the largest revenue contributor inside Credo’s optical portfolio. By management’s framing on the Q4 call, which is worth confirming against the filing rather than the auto-generated transcript, Zero-Flap is guided above $100M in FY27 as one of three optical legs each above $100M, for a total optical business above $600M. The discrete DSP and PIC legs ramp more linearly. Zero-Flap is the hockey stick, steep and back-half FY27 and FY28 weighted, because it is gated on hyperscaler qualifications converting to volume rather than on smooth quarterly shipments.

That hockey-stick shape is the source of both the upside and the risk, and I will be precise about both. The upside: an order-of-magnitude ASP advantage on the fastest-growing optical leg, ramping into a reliability problem that gets worse, not better, as clusters scale. The risk lives in the back-half timing, which is the bear case below.

The Strategic Option: A Direct Path to Co-Packaged Optics

The Dust silicon-photonics roadmap is the part of Zero-Flap the consensus model mostly overlooks, and it is low-cost optionality on the next architecture. The same silicon-photonics intellectual property that lets Credo use fewer lasers today scales across 800G, 1.6T, and a path to 3.2T network speeds. That roadmap is also the direct on-ramp to co-packaged optics (CPO) and near-packaged optics (NPO), the architectures where the optics move onto or next to the switch chip itself, with initial revenue around FY2028.

This is where Zero-Flap becomes more than a product line and starts to look like a position in the next architectural transition. The physics is the lane-speed jump from 100G to 200G per lane, which makes the laser the binding, reliability-limited component and reshuffles who captures the margin. Zero-Flap is Credo’s answer to that physics from a different layer: instead of competing to build the most reliable laser, it engineers a link that needs fewer of them. As the industry moves toward CPO, the company that already owns the DSP-to-photonics integration and the reliability software is positioned to participate rather than be displaced.

Why It Matters Technically: Reliability Becomes the Binding Constraint

As AI clusters scale toward gigawatt-class power and denser architectures, even isolated link instabilities stop being a tail risk and become the dominant driver of cluster availability. The variables that matter at that scale, cluster breakup time, GPU utilization, overall system availability, are all downstream of link reliability. Add more links and the aggregate flap rate rises. Pack them denser and thermal stress rises, which is exactly the condition lasers hate. The reliability problem does not get diluted by scale. It compounds with it. Credo calls reliability its “North Star,” and at gigawatt scale that label describes the binding constraint rather than dressing it up.

This reframes what Credo actually is. For a year the consensus model has treated Credo as an active-electrical-cable (AEC) company, a copper interconnect supplier, defending a niche against the optical transition. Zero-Flap inverts that. Credo is now selling optical transceivers directly, as a system-level reliability product, moving up from a SerDes and DSP and AEC supplier into the optical TAM long dominated by Coherent, Lumentum, and the merchant transceiver vendors. The product the market skips in the model is the one that changes what the company is.

The Bear Case

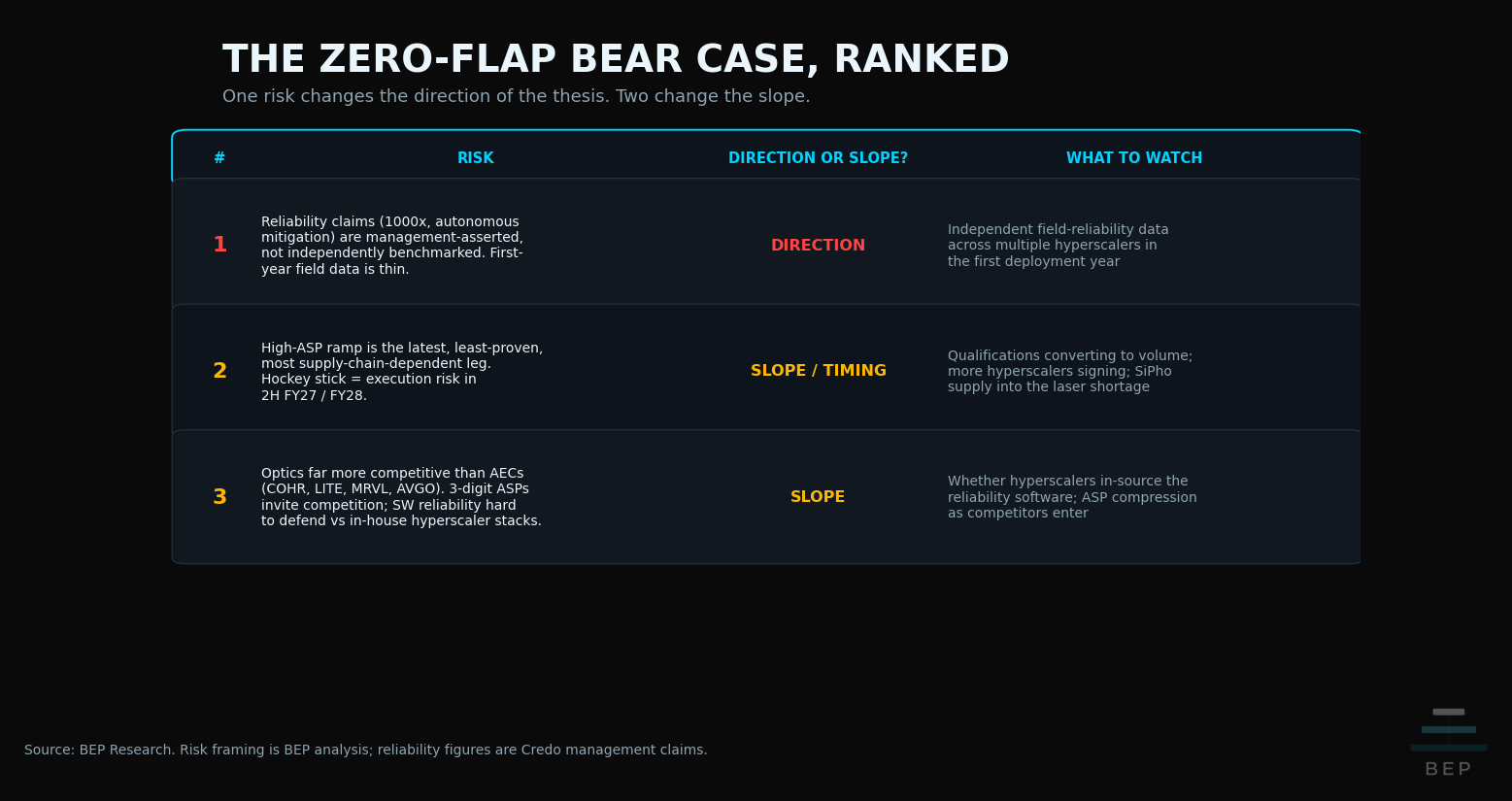

Three risks would break this thesis, and I am ranking them by what changes the conclusion versus what only changes the magnitude.

1. The reliability claims are management-asserted, not independently benchmarked. “Zero-flap” is a marketing term. The reliability and autonomous-mitigation claims come from Credo, not from a neutral third party with published field data across multiple hyperscalers. One number deserves special care: the often-quoted 1000x reliability figure belongs to Credo’s copper AECs measured against laser-based optical modules, and there is no comparable independently published figure for the Zero-Flap optical line itself, so do not carry it across. Optical reliability products live or die on the first deployment year of real-world data, and the high-ASP optical line is barely into that window. If early field data disappoints at a major customer, the system-moat story compresses fast and the stock reverts to being priced as an AEC incumbent with an optical side project. This is the risk that would change the direction of the thesis, not just the slope. It is also the risk I flagged when I corrected my own Credo view in Credo Was the Wrong Question: the Zero-Flap ramp is real, but it is a concentrated bet on one product line through the first year of field proof.

2. The high-ASP ramp is the latest, least-proven, most supply-chain-dependent leg. The hockey-stick shape means the execution risk is concentrated in the back half of FY27 and into FY28. A hockey stick that does not bend on schedule is just a flat line that disappointed. This one depends on qualification timelines holding, additional hyperscalers signing on, and the silicon-photonics supply chain delivering into a known laser shortage. This risk changes the slope and the timing, not the direction, but in a name where the ramp is the whole story, slope is most of the value.

3. Optics is a far more competitive arena than AECs, and software-defined reliability is hard to defend. In copper AECs Credo holds a dominant share. In optics it is the entrant against Coherent, Lumentum, Marvell, Broadcom, and the merchant transceiver and DSP vendors, all entrenched. Three-digit ASPs are an invitation to competition, not a moat by themselves. And the software layer, the part Credo leans on hardest as the differentiator, is exactly the kind of telemetry-and-SDK function a large hyperscaler could choose to build in-house. If the customers who most need Zero-Flap decide reliability software is something they own rather than buy, the moat thins from the most valuable end first.

So What?

Stop reading Zero-Flap as a marketing name and start reading it as the answer to the question the whole AI buildout is converging on: how do you keep a hundred-thousand-GPU cluster usefully online when the single most failure-prone part, the laser, sits in every link and the link count is going parabolic? Network reliability has quietly become the binding constraint on usable compute, the same way memory bandwidth and power density became binding constraints before it. Zero-Flap is the only optical product engineered, in hardware and software together, to attack that constraint directly.

For Credo specifically, that is why this one product line is the highest-leverage part of the story. It carries the richest ASPs, it ramps into a problem that worsens with scale, and on management’s own math it becomes the largest leg of the optical business and cheap optionality on the co-packaged-optics transition. The catch is price: even after its post-earnings drop Credo trades around 32 times trailing sales, a multiple that already capitalizes much of this optical optionality, which is why the proof matters more than the next print. I hold Credo, and Zero-Flap is the reason I read it as a multi-product optical company now rather than the copper incumbent it was a year ago. What I am watching is the first year of independent field-reliability data from the hyperscaler deployments, because that is what turns a management claim into a moat.

The market is modeling the company Credo was.

The product it skips is the one that says what Credo is becoming.

Read the reliability line, not the AEC line.

Coming Up

A follow-up deep dive on the Dust silicon-photonics roadmap and the path to co-packaged optics is in motion, pending a conversation with Credo’s optical leadership on the qualification pipeline beyond the anchor hyperscaler and the FY2028 CPO timeline. I will also be tracking the next two optical earnings prints from Lumentum and Coherent for the laser-supply read-through that sits underneath every Zero-Flap link. Paid subscribers get the optical-leadership conversation first.

Related research: The Great Photonic Divergence (why the 100G-to-200G lane jump makes the laser the binding, reliability-limited component and reshuffles the margin).

Disclosure: The author holds positions in NVDA, BE, LITE, CRDO, TSEM, LSCC, ORCL 2027 Calls, and ALAB. This is not investment advice.